The global EV transition isn’t just a technology shift — it’s also a data definition problem.

In 2024 a strange contradiction appeared in several EV reports. One widely cited analysis placed the European EV fleet at one figure, while another reputable dataset showed a significantly different total for the same region. Both reports cited official sources. Both were technically correct.

They were simply counting different things.

This problem appears constantly in EV analysis because people do not agree on what an EV actually is.

Some datasets define EV as battery electric vehicles (BEVs) only, while others include plug‑in vehicles (BEV + PHEV). China — the world’s largest EV market — uses yet another term: NEV (New Energy Vehicle), which includes:

• BEV – Battery Electric Vehicles

• PHEV – Plug‑in Hybrid Electric Vehicles

• EREV – Extended‑Range Electric Vehicles

At first glance this might seem like a minor technical detail. In reality it creates enormous confusion in EV statistics, policy discussions, and public debates.

Most major EV data agencies — including widely cited trackers such as EV‑Volumes, the International Energy Agency (IEA), and BloombergNEF — report EV data in multiple categories. Some datasets focus on BEV‑only vehicles, while others report plug‑in vehicles (BEV + PHEV).

When analysts mix these categories without clearly stating the definition being used, the same market can appear to have very different EV totals.

As someone who has been collecting and reconciling EV datasets since 2020, I can say without exaggeration that this definitional chaos has been one of the biggest obstacles to accurate analysis of the EV transition.

Authoritative datasets themselves illustrate how quickly EV adoption is growing. The IEA Global EV Outlook 2025 reports that global EV sales exceeded 20 million vehicles annually, driving rapid expansion of the global electric car stock. Independent datasets such as EV‑Volumes’ 2025 year‑end market update show similar trajectories for cumulative plug‑in vehicle adoption.

When Global Fleet Data Exposed the Problem

The scale of this problem became clear while rebuilding global EV fleet statistics.

During the reconstruction of these datasets I repeatedly encountered contradictory figures for the same markets coming from different official sources.

Some datasets were reporting:

• BEVs only

• others were reporting plug‑in vehicles (BEV + PHEV)

• some sources mixed definitions without clarifying them at all

The result was widespread under‑reporting of the true EV fleet size.

Initially, using a mixture of these datasets, I arrived at an estimate of roughly:

80 million EVs on the road globally in 2025.

However, after rebuilding the dataset from the ground up using validated official sources and forcing every market to include plug‑in vehicles (BEV + PHEV), the number increased significantly.

After months of revision, cross‑checking and verification, the global fleet figure now sits at around 90 million EVs on the road in 2025.

This scale aligns with projections from major industry sources. The IEA Global EV Outlook 2025 and EV‑Volumes market data both indicate that cumulative EV stock has expanded rapidly as global plug‑in vehicle sales accelerated during the early 2020s.

That is not a small difference.

It represents millions of vehicles that effectively disappear depending on which definition is used.

Unfortunately the problem does not stop there.

Many social media accounts and analysts unknowingly repeat mixed datasets. Because the numbers appear authoritative they often gain high traction online, spreading confusion even further.

Interestingly, China was the only major market where EV data was consistently reported.

Most other regions were a statistical mess.

Part of the problem is that even major industry data providers use slightly different reporting standards. Organisations such as EV‑Volumes, the IEA, BloombergNEF and national transport agencies often track both BEV‑only and plug‑in vehicle (BEV + PHEV) categories. However charts and summaries circulating online frequently mix these figures without clearly stating which definition is being used.

As a result, two analysts can reference “EV fleet” data from reputable sources and still arrive at very different totals depending on which definition sits behind the numbers.

In other words, the EV transition is not only a technology transition — it is also a data definition problem.

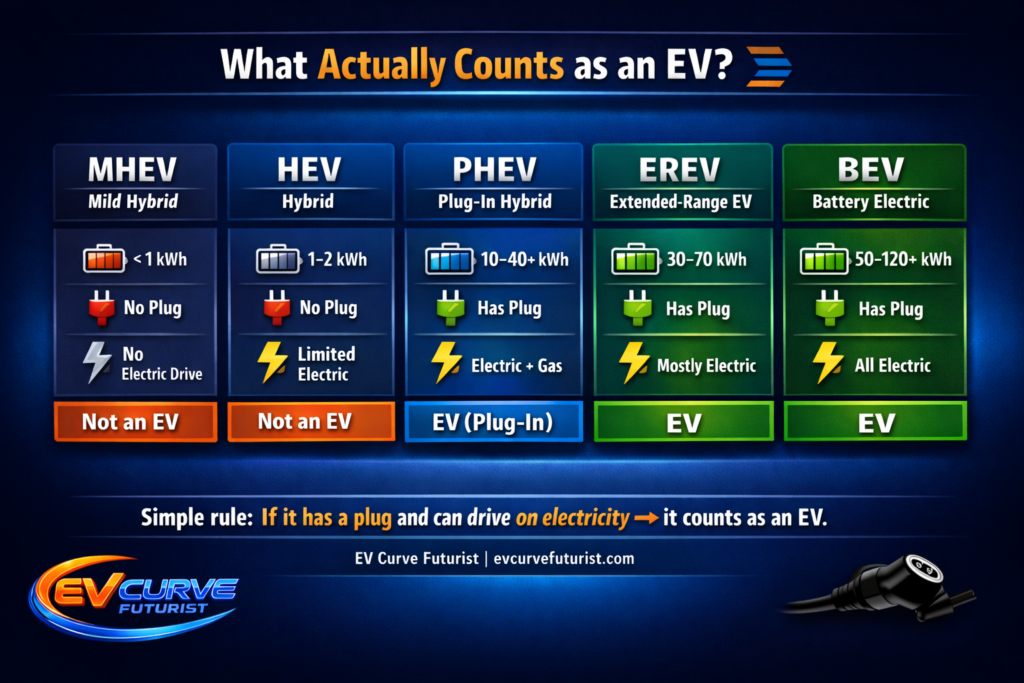

The Simple Rule: If It Has a Plug, It’s an EV

Back in 2020 I adopted a simple working definition for my datasets:

If the vehicle has a plug, it is an EV.

That means EV includes:

• BEV

• PHEV

• EREV

And excludes:

• ICE vehicles

• Mild hybrids (MHEV)

• Conventional hybrids (HEV)

Why?

Because plug‑in vehicles share three critical characteristics:

1️⃣ They can charge from the electrical grid

2️⃣ They contain meaningful battery capacity

3️⃣ They can operate in pure electric driving mode

If a vehicle cannot be plugged in and cannot drive purely on battery power, then it remains fundamentally a combustion vehicle with electrical assistance.

That is not an EV.

Why Mild Hybrids Were Removed From the EV Category

One of the most important corrections around 2020 was the removal of mild hybrids from EV classifications in many regulatory frameworks.

Mild hybrids typically contain very small batteries (often less than 1 kWh) and cannot drive on electricity alone.

Their electric systems simply assist the combustion engine.

Yet for years many automakers marketed these vehicles as “electrified.”

In some markets this allowed them to qualify for:

• emissions credits

• regulatory exemptions

• consumer subsidies

Placing mild hybrids in the EV category created enormous statistical distortion.

Removing them and placing them firmly back in the ICE category was a critical step toward clarity.

The Rapid Evolution of Plug‑In Hybrid Technology

Another reason the EV definition debate has become more complicated is that plug‑in hybrid technology has evolved dramatically.

Early PHEVs typically had:

• 8–12 kWh batteries

• 40–60 km electric range

Today, many Chinese plug‑in platforms carry:

• 30–70 kWh batteries

• 200–400+ km electric range

Some modern EREV platforms can deliver 400–500 km of pure electric driving before the generator activates.

In other words, some plug‑in vehicles now carry battery capacities similar to BEVs from only a few years ago.

This evolution complicates the simple narrative that only BEVs are “truly electric” and highlights how quickly drivetrain architectures are converging.

Of course, real‑world usage still matters. A plug‑in vehicle that is never charged will behave much like a hybrid.

But from a technology and infrastructure perspective, the presence of the plug still matters — it connects the vehicle to the electrical system and enables electric driving when used properly.

There is also a valid criticism often raised about plug‑in hybrids: many are not charged regularly.

Several real‑world studies have examined this issue. Research from the International Council on Clean Transportation (ICCT) found that real‑world fuel consumption of company‑car PHEVs can be three to five times higher than official test values. Analyses by Transport & Environment (T&E) and research from the Fraunhofer Institute similarly show that many PHEVs are charged far less frequently than policy models assume.

Some datasets suggest company‑car PHEVs may be plugged in as little as 25–30% of the time.

When this happens, they effectively operate as conventional hybrids.

However this is fundamentally a usage problem, not a definition problem.

The vehicle can charge.

It has a plug.

For tracking grid connection points, battery capacity deployed, and technological adoption, that still matters.

Why the EV Definition Became So Confusing

Several factors contributed to this confusion.

1. Legacy Automakers Protecting Market Share

Western automakers heavily promoted hybrid categories as a way to delay full electrification while still appearing compliant with emissions regulations.

This allowed them to continue selling combustion vehicles while marketing them as “electrified.”

2. Policy Lag and Government Misunderstanding

Early government regulations often failed to distinguish between:

• mild hybrids

• full hybrids

• plug‑in hybrids

• BEVs

This bureaucratic lag created years of statistical inconsistency.

3. BEV‑Only Advocacy

Some commentators argue that EV should mean BEV only.

Their reasoning usually centres on lifecycle emissions, the continued presence of combustion engines in PHEVs, and the desire to accelerate a full transition away from fossil fuels.

Those arguments are understandable.

However, from a data and system‑transition perspective, excluding plug‑in vehicles creates a different problem: it hides a large portion of the electrification that is actually occurring in the fleet.

For tracking battery deployment, electricity consumption and oil displacement, plug‑in vehicles remain a meaningful part of the transition.

4. Marketing Terminology

The automotive industry widely adopted the vague marketing term “electrified vehicles.”

This umbrella category often includes everything from mild hybrids to full BEVs.

From a technical perspective, this classification is almost meaningless.

5. Dealer‑Level Consumer Confusion

In many markets dealerships still sell mild hybrids while implying consumers are purchasing electric vehicles.

In reality these vehicles remain fundamentally combustion‑powered.

What This Means For The EV Transition

For Policymakers

Subsidies, emissions regulations, and charging infrastructure planning all depend on understanding which vehicles actually connect to the electrical grid.

For Investors

Battery demand forecasts and mineral supply projections change dramatically depending on whether plug‑in hybrids are included in EV datasets.

For Consumers

Understanding what “EV” actually means helps prevent the common dealership bait‑and‑switch where mild hybrids are marketed as electric vehicles.

China Solved This Problem Years Ago

China addressed this definitional issue by introducing the NEV (New Energy Vehicle) category.

NEV includes all plug‑in vehicles:

• BEV

• PHEV

• EREV

This definition aligns with the real technological shift occurring in transport:

vehicles powered primarily by electricity and supported by batteries.

The Bottom Line

The EV transition is complex enough without definitional confusion.

A simple rule provides clarity:

If the vehicle has a plug and can drive on electricity, it is an EV.

This approach aligns with the definition used in the world’s largest EV market, acknowledges how rapidly vehicle technology is evolving, and provides a consistent framework for tracking fleet electrification.

Most importantly, it ensures the data reflects what is actually happening on the road.

When I corrected for definitional inconsistencies in my own dataset, something remarkable happened.

The global EV fleet estimate increased from roughly 80 million vehicles to around 90 million vehicles.

Ten million vehicles appeared almost overnight.

Those vehicles were always there.

They simply were not being counted because different datasets were using different definitions.

In a transition this important, that is not acceptable.

And that is exactly why clear definitions matter.

Reader Discussion

Do you include plug‑in hybrids when analysing EV adoption?

Definitions shape the numbers — and the story the data tells.

Share your view and compare how different datasets treat plug‑in vehicles.

A simplified EV fleet reconciliation template will be shared via EV Curve Futurist so readers can explore how different EV definitions change the numbers.