When transport systems change, history doesn’t ease into it — it snaps.

The shift from horse to car wasn’t gradual or polite. Cities rebuilt themselves in a single generation. Entire industries vanished. New ones emerged almost overnight.

The transition from internal combustion engine (ICE) vehicles to electric vehicles (EVs) follows the same pattern. Once a new system becomes cheaper, simpler, and superior, the old one doesn’t slowly decline — it collapses far faster than intuition expects.

This isn’t a future projection. It’s already underway.

1. From Engines to Systems

Internal combustion vehicles were mechanical compromises — thousands of moving parts, constant maintenance, volatile fuel inputs, and low efficiency. EVs replace this with something fundamentally different: electric drivetrains integrated into software-defined systems.

That shift collapses complexity:

- fewer moving parts

- minimal servicing

- higher energy efficiency

- software-driven optimisation

Once transport becomes electric, it stops being a fuel problem and becomes an energy, storage, and software problem — and those scale exponentially.

2. Economic Trigger

Large systems don’t transition because of intent, politics, or good intentions.

They transition when underlying cost structures cross hard economic thresholds.

In transport, that trigger is battery economics.

For decades, electric vehicles were technically viable but economically marginal — heavier, more expensive, and constrained to niche use cases. That changed once lithium-ion battery manufacturing reached industrial scale and learning curves began to compound. As costs fell, EVs didn’t improve linearly — they crossed a threshold.

For years, that threshold was framed at ~$100 per kWh at the pack level. This wasn’t an arbitrary number — it marked the point at which EVs could compete across mass-market segments on total cost, not just on fuel and maintenance.

What has now become clear is that this threshold has not just been reached — it has been passed.

Updated 2025 production-weighted data shows global battery pack costs clustering closer to ~$90 per kWh, particularly as LFP and China-led manufacturing dominate volume. This does not redefine the trigger — it confirms that the system is now operating beyond it.

Once the $100/kWh barrier is broken, adoption no longer needs incremental policy support. Economics take over. Volume accelerates. Supply chains flip.

This is the point at which internal combustion breaks — not gradually, but structurally.

The chart below shows the causal relationship clearly: battery costs fall first, and NEV adoption responds second. Temporary shocks — inflation, supply-chain disruptions, or commodity volatility — create noise, but they do not change the direction once the trigger is passed.

$100/kWh was the gate.

$90/kWh is the proof that we’re already through it.

“Battery costs shown are global, volume-weighted averages across EV and stationary markets.“

Once the trigger is pulled, outcomes become inevitable. Everything that follows — ICE sales collapse, OEM disruption, supply-chain rewiring — is an effect, not a cause.

2. Hybrids, PHEVs & EREVs: A Gradient of Electrification

Not all EVs disrupt equally.

Mild and full hybrids (MHEV / HEV) remain combustion-led, with electrification playing a supporting role. Plug-in hybrids (PHEV) and extended-range EVs (EREV) can drive electrically and charge from the grid, but still retain combustion systems — making them EVs, but transitional.

This is why PHEVs and EREVs are classified here under the EV (or NEV) umbrella: they materially displace fuel use, even if they are not the end state.

Only battery-electric vehicles (BEVs) remove the engine entirely. That removal collapses complexity, cuts maintenance, and enables software-defined, autonomy-ready transport.

Hybrids optimise the old system.

PHEVs and EREVs bridge away from it.

BEVs end it.

4. The Second-Hand EV Effect

One of the most misunderstood dynamics in transport disruption is the role of used EVs.

EV adoption doesn’t stall when new sales slow — it accelerates as vehicles cascade into the second-hand market. Lower purchase prices combine with dramatically lower running costs, pulling in buyers who would never consider a new car.

This creates a reinforcing loop:

- new EVs scale production

- used EV prices fall

- adoption broadens

- charging and service ecosystems expand

This is how disruption escapes early adopters and becomes structural.

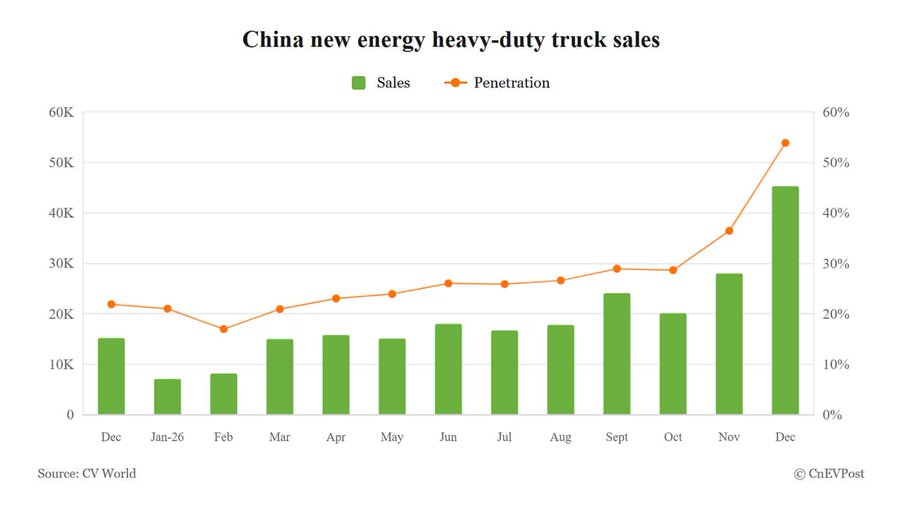

5. EV Trucks: The Next Demand Shock

This is where electrification stops being debatable. Passenger cars introduce the transition; heavy trucks force it.

Passenger cars were only the opening act.

China has now crossed a critical threshold in the most cost-sensitive transport segment on Earth. In 2025, electric heavy-duty truck sales reached 231,100 units (+182% YoY), with annual penetration rising to 28.9% (vs 13.6% in 2024) and monthly penetration briefly exceeding 50% (53.9%). This is not cars or buses — this is heavy freight, where economics dominate ideology.

The reason is scale and utilisation.

Typical battery sizes in China’s electric heavy-duty truck fleet are far larger than passenger EVs:

- Urban / short-haul: ~200–300 kWh

- Regional haul (most volume): 300–450 kWh

- Battery-swap trucks: ~280–320 kWh per standard pack

- Mining, ports, extreme duty: 500–600+ kWh

That is 5–8× a passenger EV battery, deployed into vehicles that run higher daily utilisation, cycle batteries harder, and prioritise uptime and total cost of ownership. This is why LFP dominates.

Battery swapping completed the equation. Standardised packs, 5–10 minute swaps, and battery ownership separated from the vehicle removed upfront capex while maximising utilisation. Fleets now save ~RMB 1–1.2 million per truck over 8–10 years versus diesel. At that point, diesel isn’t conservative — it’s risky.

This is the lithium demand shock most models miss. One electric heavy truck represents multiple passenger EVs’ worth of batteries, purchased on fleet cycles, locked into infrastructure, and deployed immediately. There is no smooth adoption curve here — only step changes.

When heavy trucks tip, diesel demand destruction accelerates, battery demand compounds faster than car-centric assumptions, and lithium doesn’t drift — it reprices.

6. Safety, Fire Risk & Reality

Few narratives are more distorted than EV battery fires.

Yes, EVs can burn. So can ICE vehicles — far more frequently. What matters is rate, severity, and controllability, not anecdotes.

As battery chemistries evolve (especially LFP) and thermal management improves, EV fire risk continues to fall — even as fleet size explodes. The gap between perception and data remains wide — but it is closing.

7. China: Where ICE Ends First

China is not transitioning — it is exiting.

With EVs already dominating urban sales, policy aligned with cost curves, and domestic manufacturers scaling at industrial speed, the internal combustion engine is approaching end-of-life in the world’s largest auto market.

This matters globally. When China moves, supply chains move. When supply chains move, legacy automakers elsewhere don’t get a vote.

The pace of this “snap” will vary by region — shaped by grid investment, industrial policy, and consumer preferences — but the direction does not. China is the leading indicator, not the exception.

Norway deserves special mention: having led the transition for over a decade, it now sits at ~98% EV penetration in new car sales, offering a clear preview of the end state once infrastructure, incentives, and consumer confidence fully align.

8. The Endgame: 90%+ Adoption

Transport disruption follows the same pattern as every major technological shift:

- slow start

- rapid inflection

- sudden dominance

Once EVs cross cost parity — not just upfront, but lifetime — resistance collapses quickly. Infrastructure fills in after adoption, not before.

This is why projections that assume gradual linear change keep missing reality.

9. Autonomy, TaaS & the End of Ownership

Electrification is only the first unlock. Autonomy is the force multiplier.

Once vehicles are electric, software-defined, and connected, full self-driving becomes an engineering problem — not a science experiment. Transport shifts from a product to a service.

Autonomous trucks transform highways through 24/7 utilisation and lower freight costs. Robotaxis reshape cities through cheaper point-to-point mobility, fewer parked cars, and reduced congestion.

When utilisation replaces ownership as the economic driver, cars stop being idle assets and become networked infrastructure.

Ownership doesn’t decline because of ideology — it becomes irrelevant.

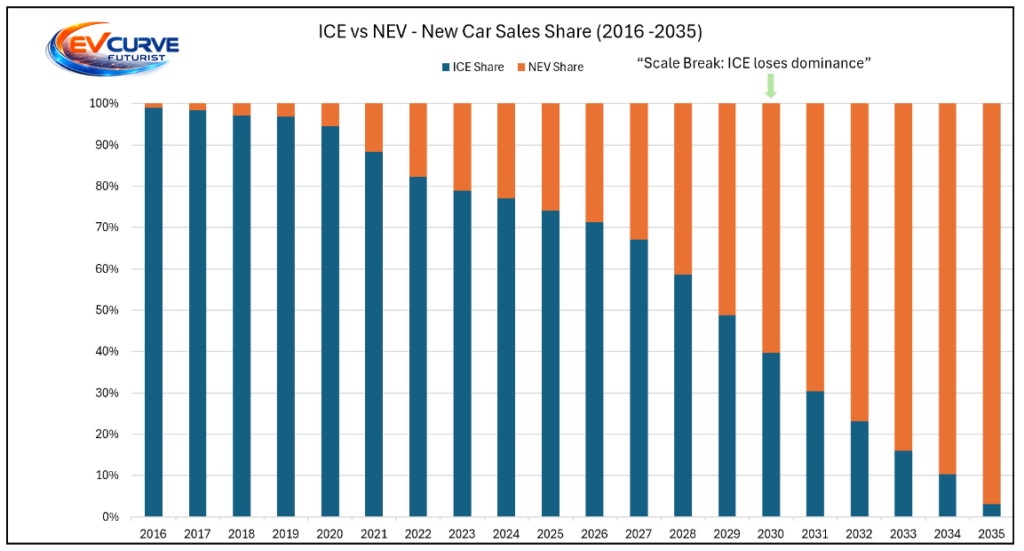

The Data Behind the Transition

Pause here. Everything above explains why transport electrifies. The charts below and my data table below show when the system breaks, and how quickly the shift compounds once scale takes over.

Narratives explain direction. Data explains inevitability.

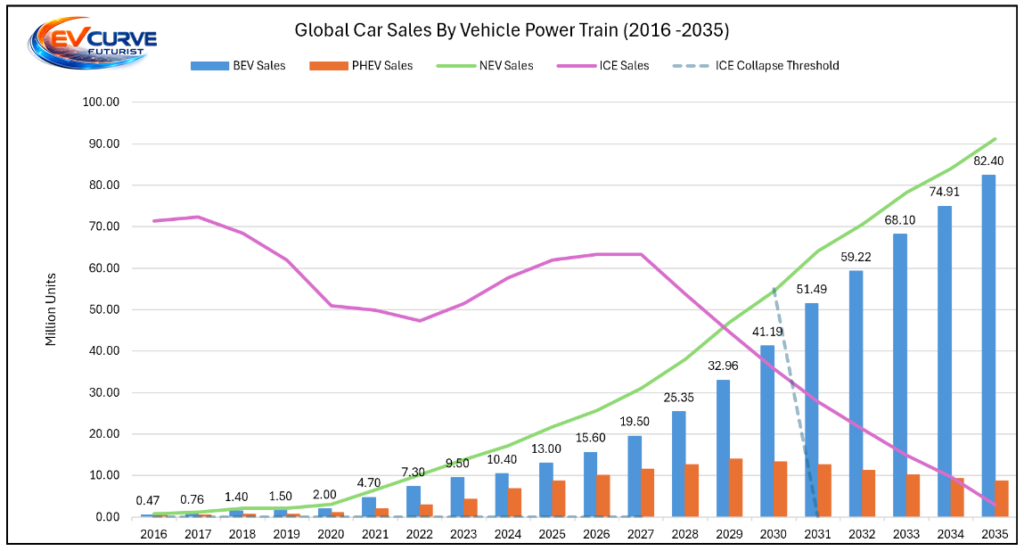

“This chart shows the zero-sum transition in new car sales. Once ICE loses scale dominance, decline accelerates non-linearly.“

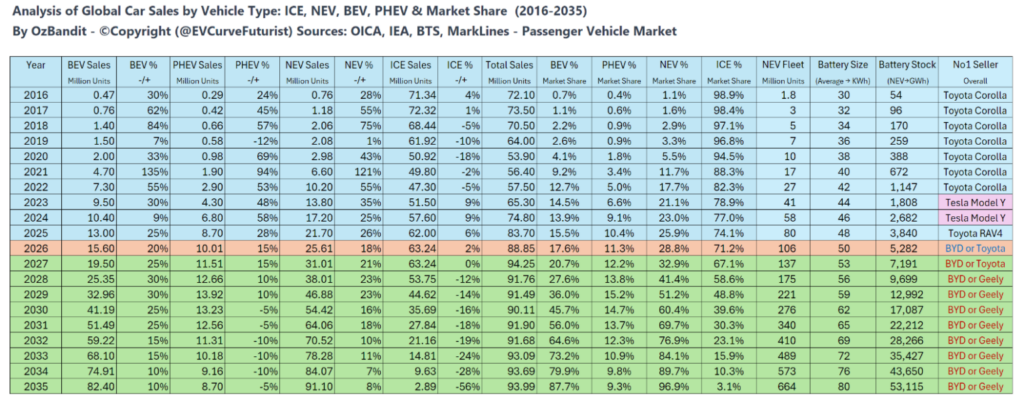

The chart and table below quantify the global passenger vehicle transition from 2016 to 2035 using annual sales, market share, cumulative fleet size, average battery capacity, and total EV battery stock.

Pay close attention to battery size growth, cumulative battery stock, and NEV fleet size. These are the compounding variables most EV forecasts still underweight — and the ones that ultimately determine scale, speed, and system impact.

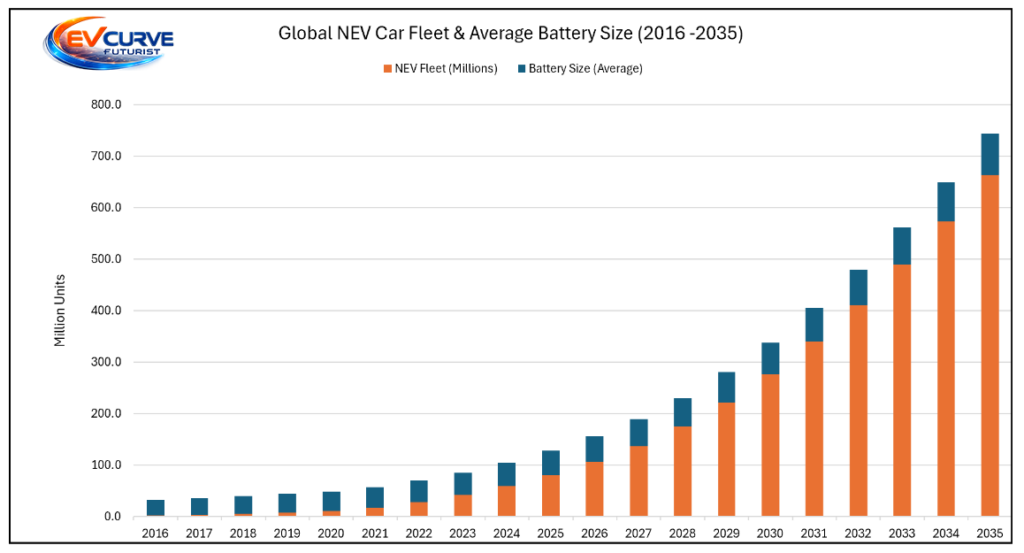

“This chart shows why electrification accelerates even without exponential sales growth. As the global NEV fleet compounds and average battery capacity rises, total battery demand scales non-linearly — driving material demand, grid coupling, and the rapid erosion of combustion economics.”

Read both charts left to right. The story is not linear growth — it is a compression of time, where adoption accelerates, ICE volume loses scale support, and decline becomes non-linear.

Two waypoints are worth noting in the data.

- By 2030, NEVs reach ~60% share and BEVs ~46%, marking the inflection point where combustion loses scale dominance.

- By 2035, NEVs reach ~97% share and BEVs ~88%, signalling system dominance, with ICE relegated to residual niches.

These outcomes are not assumptions. They fall directly out of the sales, fleet, and battery stock trajectories shown.

The dashed ICE Collapse Threshold marks the point at which combustion platforms irreversibly lose scale advantages, supplier leverage, resale value, and capital access — triggering nonlinear decline.

What the Data Ultimately Tells Us

Taken together, the data leads to several unavoidable conclusions:

1. The transition is demand-led, not policy-led.

EV adoption accelerates without requiring aggressive bans or mandates. Cost curves, scale efficiencies, and product superiority dominate.

2. ICE does not lose gradually forever — it loses abruptly once scale breaks.

Legacy volume sustains ICE temporarily, but once NEVs dominate new sales, combustion economics unravel quickly.

3. Hybrids are a bridge, not a destination.

PHEVs expand during the transition, then peak and decline as BEVs remove their remaining advantages.

4. Battery scale becomes the true constraint — and the true signal.

By the early 2030s, battery stock growth, not vehicle count, becomes the limiting factor, shifting focus to materials and manufacturing capacity. At that point, transport planning starts to resemble energy system planning.

5. Transport is no longer a standalone sector.

As EV fleets scale, transportation becomes tightly coupled to electricity systems, storage, grids, and energy security.

6. The end state is system dominance, not symbolic 100% adoption.

Residual ICE persists in niches, but electrified vehicles set the economics, standards, and direction of the system.

The Thesis, Distilled

Transportation is electrifying because it is cheaper, simpler, and superior — not because it is mandated.

EVs aren’t replacing cars. They’re replacing an entire system built around combustion, maintenance, and fuel scarcity.

Once transport runs on electrons, it becomes software-defined, grid-integrated, storage-linked, and autonomy-ready.

The end of combustion is not the goal — it is the precondition.

Welcome to the age of Bettrified mobility.