The Shift

Tesla’s robotaxi push is now live in Austin. It matters. But the metric has shifted. This is no longer about proving autonomy works. It is about proving it works at scale, at low cost, with short wait times. That benchmark is no longer Waymo. It is China.

Economics

Baidu Apollo Go, Pony.ai, and WeRide are not running pilots. They are running systems. Large fleets, millions of rides, and rapidly falling costs. The conversation has moved from capability to economics.

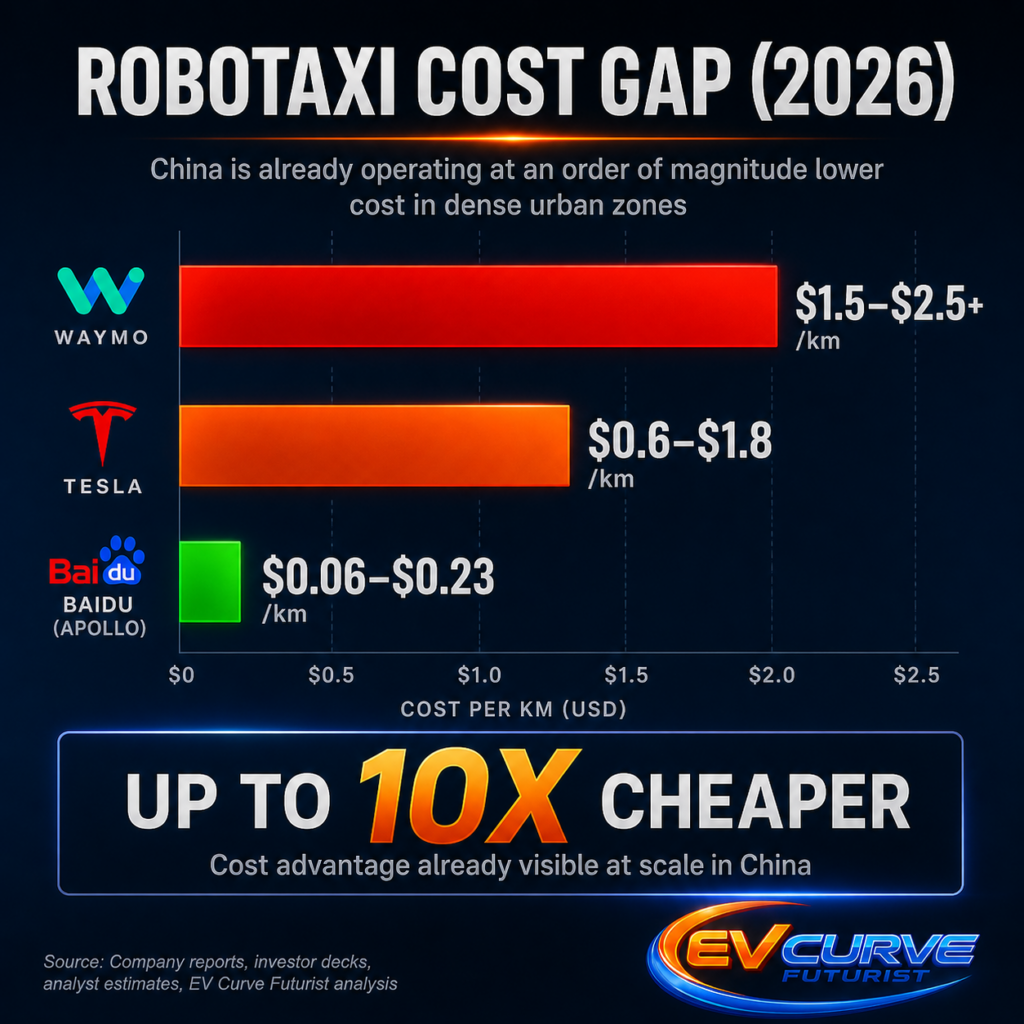

Early pricing signals show Tesla landing somewhere around $0.60 to $1.80 per kilometre, with Waymo often sitting higher depending on market. In contrast, Baidu Apollo Go is already operating in the $0.06 to $0.23 range in dense urban zones, with Pony and WeRide not far behind.

The gap is not marginal. It is structural.

These costs are emerging in dense, highly optimised urban environments, supported by favourable regulation and, in some cases, subsidised rollout phases. Lower labour costs, including remote safety monitoring, also contribute. These conditions are not directly comparable to early-stage deployments in sprawling US cities like Austin.

Caption: The cost gap is no longer theoretical. In dense urban deployments, Chinese robotaxi operators are already achieving dramatically lower per-kilometre costs. This isn’t incremental improvement. It’s a structural shift driven by scale, density, and continuous real-world deployment.

Caption: China isn’t experimenting with pricing. It’s compressing it. In dense urban zones, robotaxi costs have already dropped to a fraction of Western equivalents, shifting the battleground from technology to economics.

Hardware

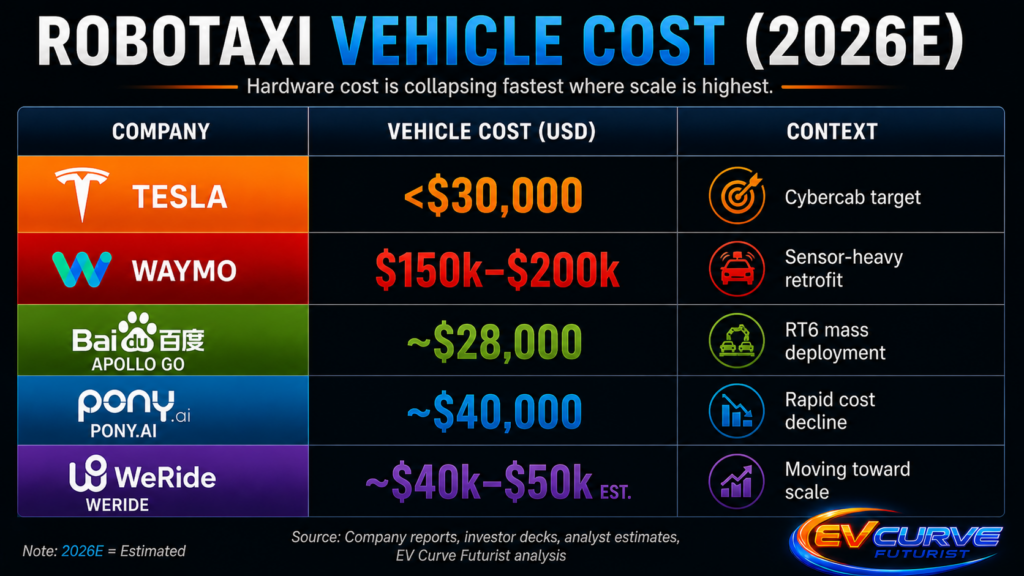

On the hardware side, Tesla’s Cybercab target under $30,000 is compelling. But China is not behind here either. Baidu’s RT6 platform is already around that level, purpose-built for autonomy and designed for mass deployment. Pony.ai and others are rapidly driving costs down through iteration and scale. The idea that China is trailing on vehicle economics no longer holds. They are already producing at the level Tesla is aiming for.

Caption: Hardware is no longer the bottleneck. Purpose-built autonomous vehicles in China are already approaching mass-market price points, matching or undercutting Western targets before full-scale rollout.

Caption: The difference is no longer capability. It’s scale. While US deployments remain concentrated in a handful of cities, China is building multi-city robotaxi networks. This shift from pilot fleets to connected systems is what drives utilisation, data, and ultimately cost advantage.

Deployment

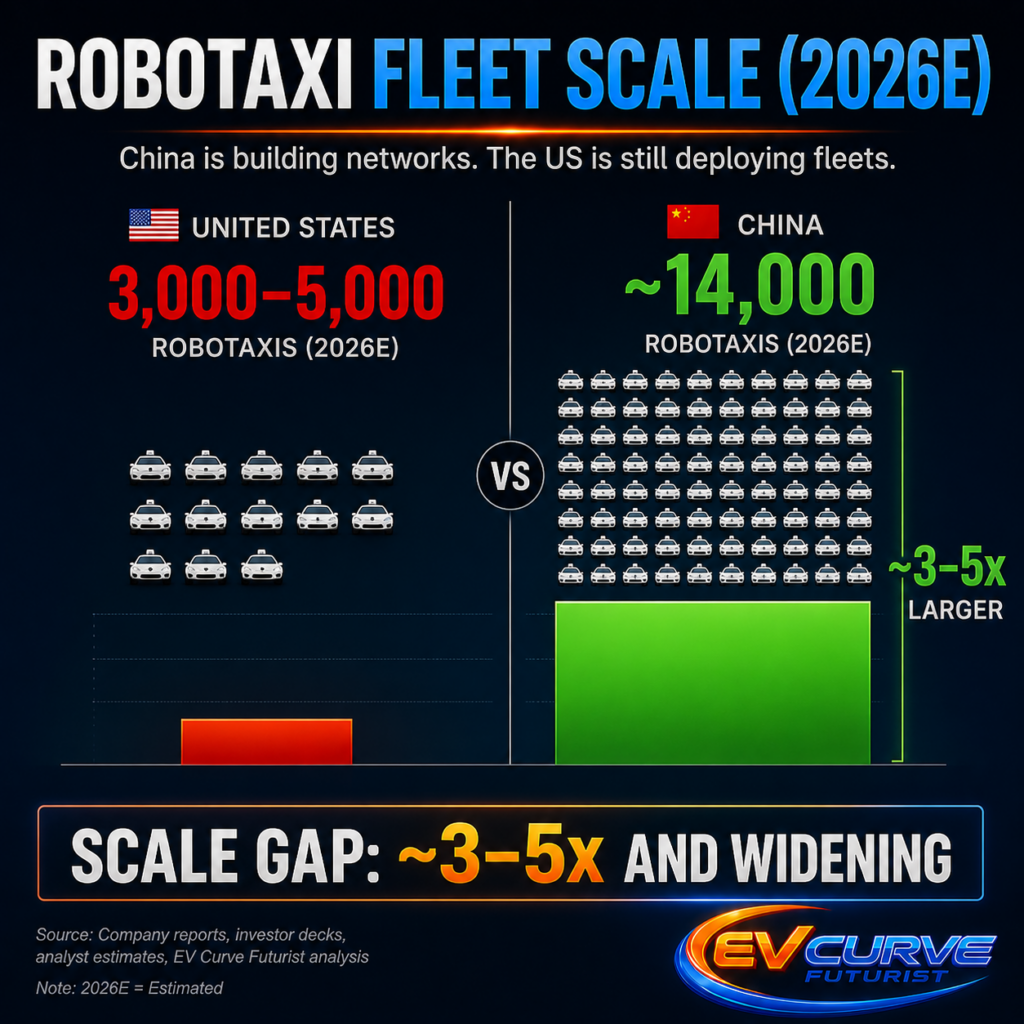

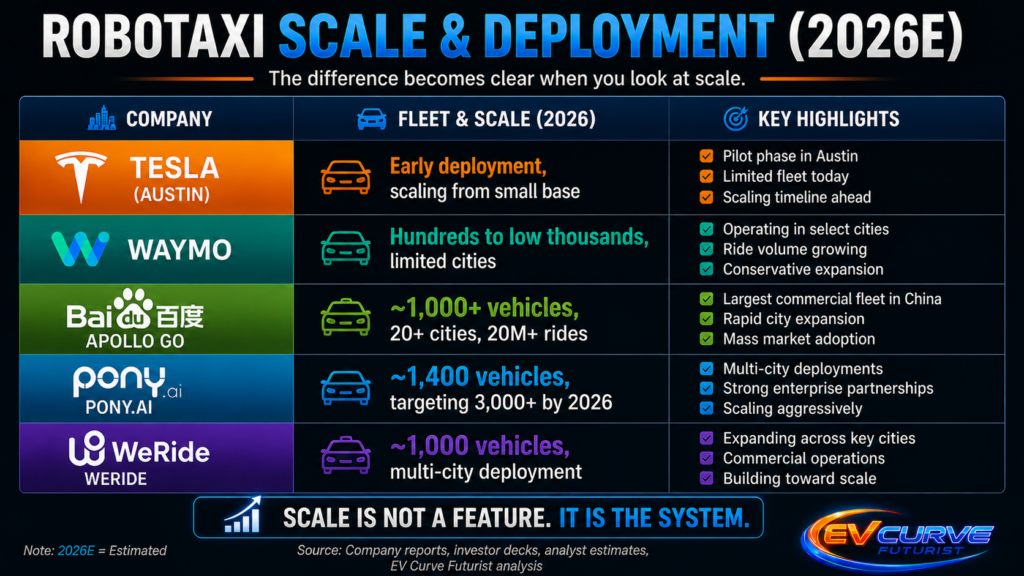

The real gap shows up in deployment. Tesla remains in limited rollout, expanding gradually. Waymo operates in select cities with hundreds of vehicles.

Baidu Apollo Go is already operating fleets in the ~1,000+ vehicle range across more than 20 cities, with 20M+ cumulative rides and roughly ~250k–300k weekly rides, and growing fast. Pony.ai has scaled to roughly ~1,400 vehicles and is targeting 3,000+ by the end of 2026. WeRide is also operating fleets in the ~1,000 vehicle range across multiple cities. This is no longer pilot scale. This is early network scale.

Meanwhile, Chinese operators are scaling across urban networks, not just test zones.

This is no longer about who has the best model. It is about who has the largest, most active system in the real world.

Caption: This is the scale advantage taking shape. China’s robotaxi fleets are expanding across multiple cities, while US deployments remain limited. A 3–5× gap at this stage isn’t just a lead. It’s the foundation of a compounding advantage.

Caption: This is where the gap becomes visible. Western deployments are measured in pilots. China is operating networks. Fleet size, ride volume, and city coverage are compounding into a structural advantage.

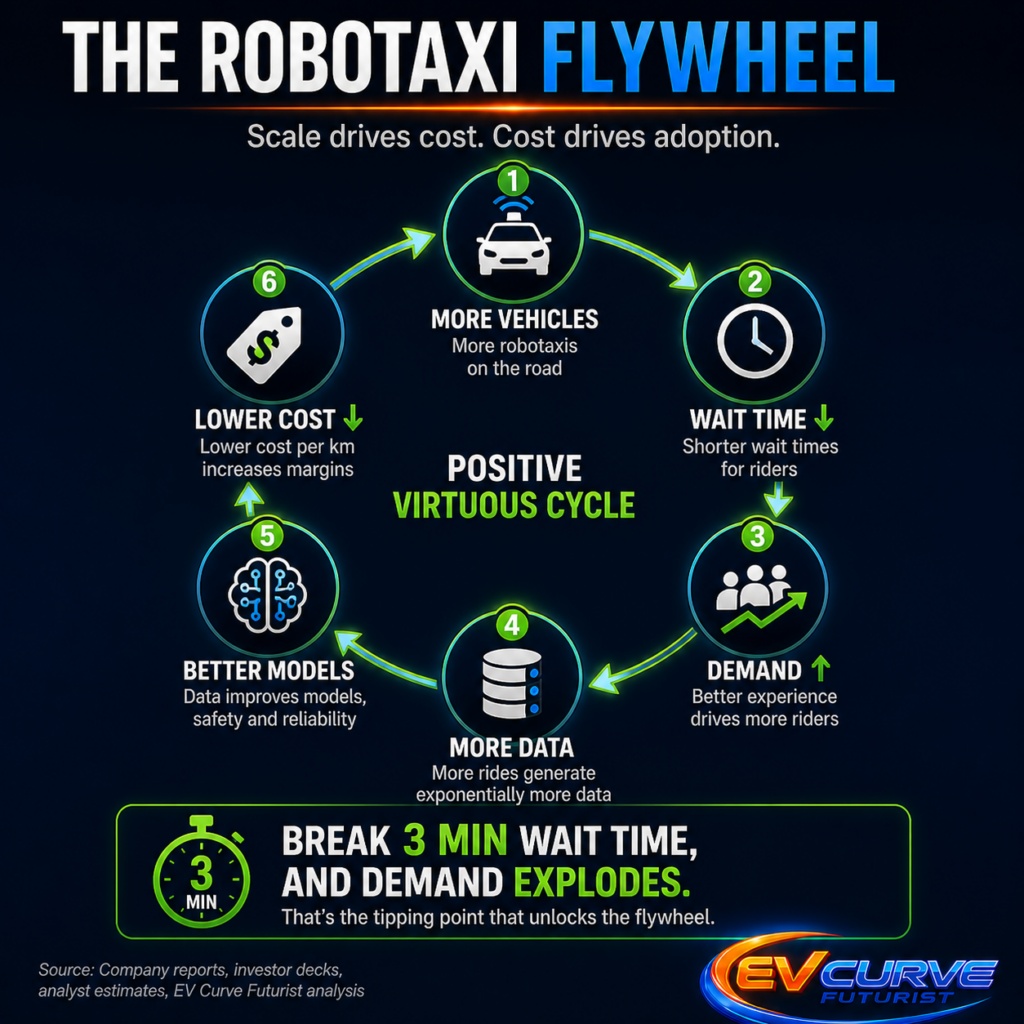

Caption: This is the robotaxi flywheel in action. Scale reduces wait times, faster pickups unlock demand, and rising demand feeds the data loop that improves performance and lowers cost. Once the flywheel spins, growth stops being linear. It compounds.

Caption: This is the tipping point in the robotaxi flywheel. Above ~3 minutes, demand builds slowly as waiting still feels like friction. Drop below it, and the experience shifts to “instant.” That’s when behaviour changes, usage accelerates, and the system moves from gradual growth to rapid adoption.

Density

Robotaxis do not win on autonomy alone. They win on density. More vehicles reduce wait times. Lower wait times increase demand. Higher demand generates more real-world data. More data improves models. Better models reduce cost. Lower cost drives more adoption.

This is the flywheel.

Sub-three-minute wait times are the tipping point. That is when robotaxis stop feeling like a novelty and start replacing private car usage. China is already moving toward that threshold in dense urban zones. The West is still building toward it.

Caption: These are two fundamentally different paths to autonomy. One optimises for scale within defined environments, driving rapid deployment and lower costs today. The other aims for generalised capability across all conditions, prioritising long-term flexibility. The outcome will depend on which approach reaches sustainable scale first.

Technology

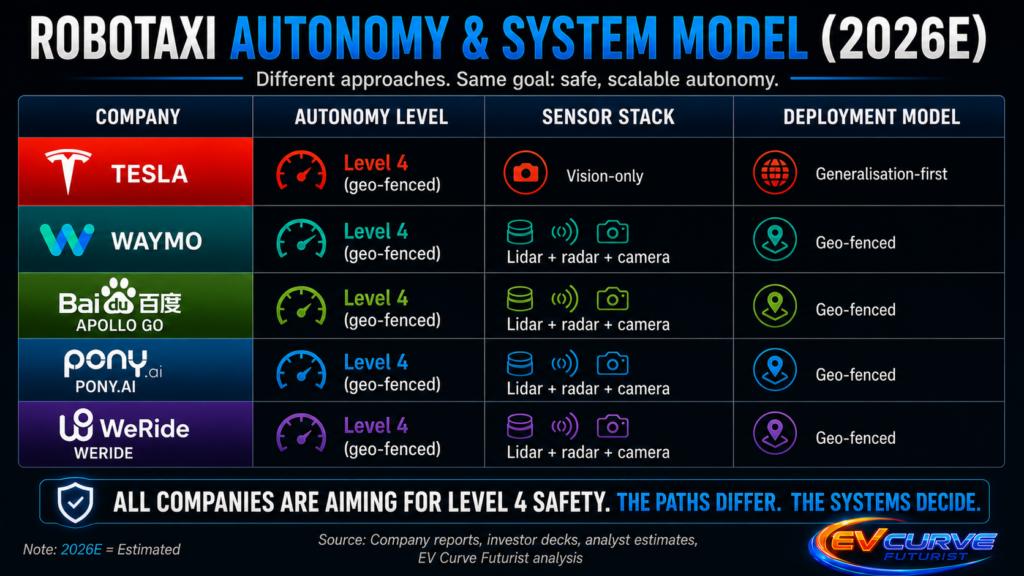

On the technology side, Tesla’s vision-only approach remains the outlier. China, Waymo, and others continue to deploy multi-sensor stacks with lidar, radar, and cameras to maximise redundancy and reliability.

Tesla’s counterargument is clear. A vision-first system, trained on vast real-world driving data, may ultimately generalise better across environments without reliance on geofencing or expensive sensor stacks. If successful, this approach could unlock lower long-term costs and broader scalability beyond tightly controlled zones.

The debate is no longer philosophical. It is practical. The question is which system scales faster, safer, and cheaper in real-world conditions.

Safety data remains uneven across regions. Disengagement rates, incident reporting standards, and transparency differ, making direct comparisons difficult. For example, Chinese operators have reported improving disengagement performance over time, though methodologies differ from US reporting, making apples-to-apples comparison challenging. That said, large-scale deployment itself becomes a form of validation over time.

Remote safety operators are another factor. Lower labour costs and centralised monitoring improve near-term economics, but reliance on human oversight may become a bottleneck as systems scale toward full autonomy.

So far, the advantage in real-world deployment is coming from systems optimised for specific environments rather than generalised autonomy.

Caption: The industry has largely converged on redundancy. Multi-sensor stacks dominate real-world deployments, while vision-only remains the outlier. The question is no longer ideology, but which system scales safely in complex environments.

Geopolitics

There is also a geopolitical layer. US restrictions on advanced semiconductor exports to China may influence long-term AI training and compute access. China’s domestic supply chain push could offset some of these constraints over time, but the balance of compute, policy, and capital will shape how fast each system scales. The real question is which can translate deployment into sustainable economics across different environments.

Timeline

The tipping point is likely not immediate, but it is approaching. If current trends hold, dense urban robotaxi networks in China could reach true mass adoption conditions before 2027. Broader global convergence, including more complex and less dense geographies, is more likely closer to 2028–2030. The race is no longer about first deployment. It is about when scaling advantages become irreversible.

What to watch in 2026–2027

- Wait times in Wuhan and Shenzhen crossing below 3 minutes

- Tesla Cybercab production timeline vs Baidu RT6 volumes

- Expansion of multi-city networks beyond core pilot zones

- Any regulatory response to Chinese robotaxi exports

Conclusion

Tesla’s robotaxi rollout is an important step, but it is no longer the leading edge. China has already crossed into scaled operations. Costs are lower. Fleets are larger. Data is compounding faster.

But those advantages are currently strongest in dense, highly optimised urban environments, not universally across all geographies.

This is not simply a question of who has the best technology. It is a question of which system can translate deployment into sustainable economics at scale across different environments.

Tesla is pursuing a generalised autonomy path that could, if successful, leapfrog geofenced systems. China is executing a deployment-first strategy, optimising for cost, density, and rapid iteration within defined zones.

One is scaling within constraints. The other is attempting to remove them.

The outcome will not be decided by capability alone. It will be decided by which approach converges on low cost, high density, and broad applicability first.

That is the real race.

Sources

- Reuters – Driverless future gains momentum with global robotaxi deployments

- Reuters – China tightens oversight after autonomous vehicle incidents

- Apollo Go / Wuhan pricing context (Robotaxi overview)

- Pony.ai cost reductions and AV economics (Nature/industry summary)

- Waymo / AV safety performance (peer-reviewed analysis)

- Market comparison of US ride-hailing pricing vs China robotaxi costs