The conversation around electric trucks used to be simple.

- They’ll never go far enough!

- They’ll never match diesel!

- They’ll never work for long haul!

- They’ll defy the laws of physics!

Those arguments are now over. The data has moved on.

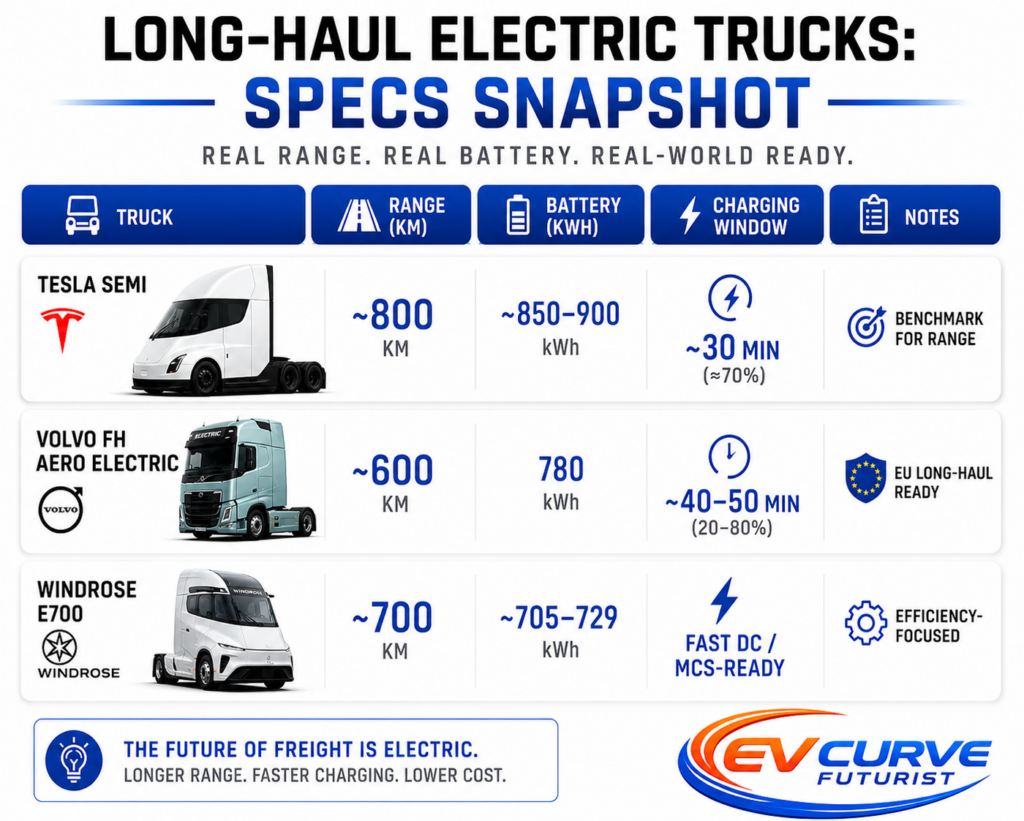

Today, multiple electric semi-trucks are pushing past 600 km of range, with some already approaching or exceeding 800 km. Not prototypes. Not concepts. Real machines now entering fleets across the United States, Europe, and China.

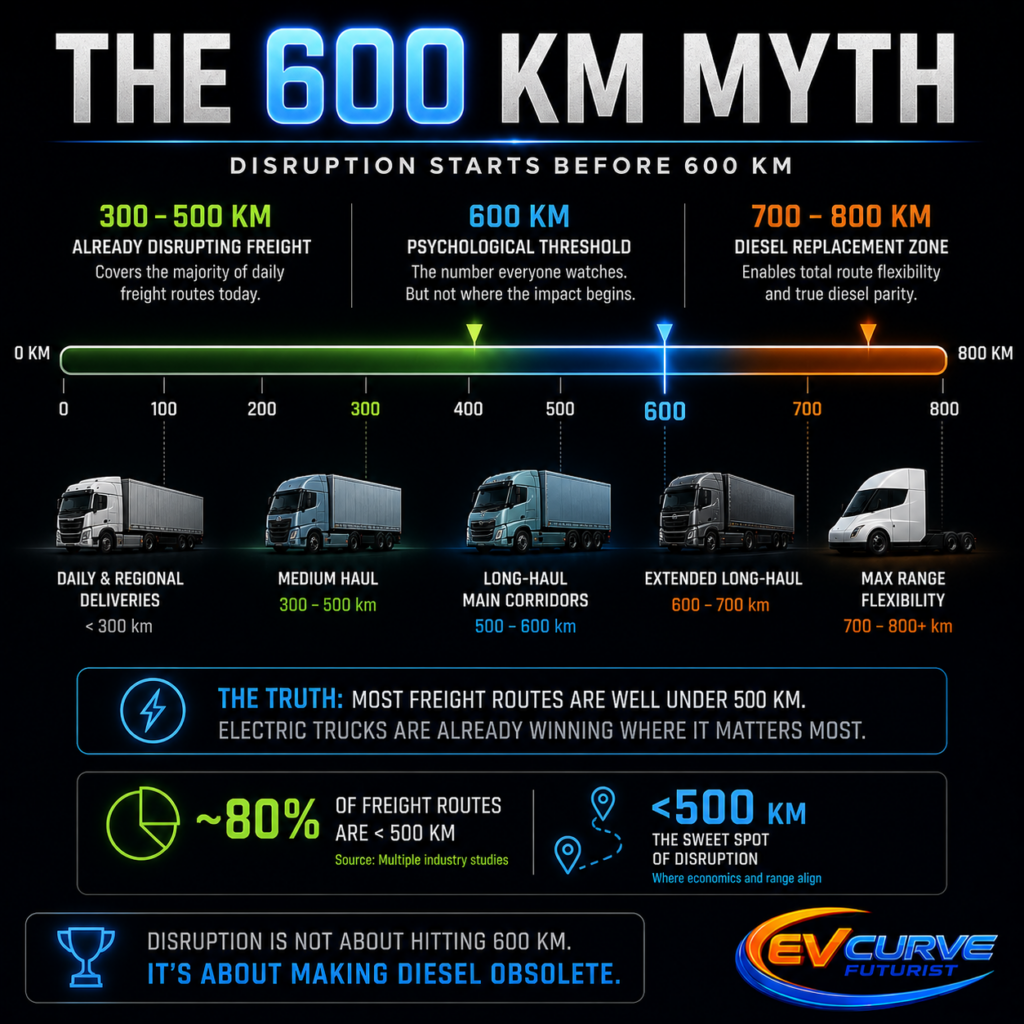

But here’s what most people are missing. 600 km doesn’t start the disruption. It just ends the debate.

The 600 km Class (and Approaching)

Across three continents, heavy-duty electric trucks are now operating in the same range class as diesel for long-haul use.

600 km Class Electric Semi Trucks (Specs)

Note: This table includes trucks that reach or approach the 600 km threshold under defined conditions .

In the United States, the Tesla Semi is leading the charge with a claimed range of around 800 km. Early deployments with companies like PepsiCo are already underway, with production scaling through 2026. Of course, manufacturer range claims versus real-world, all-weather, full-load operation is still a gap, and megawatt charging needs to exist along corridors to support it. The truck is no longer the weakest link. The infrastructure is, and that is a solvable problem.

In Europe, legacy manufacturers have moved decisively into the long-range category. Volvo’s FH Aero Electric, Renault’s E-Tech T, and Scania’s long-range electric platform are all targeting the 600 km threshold, supported by growing megawatt charging infrastructure.

Meanwhile in China, new entrants like Windrose and established industrial giants like SANY are pushing aggressively into the 600 to 700 km bracket, with a clear strategy to expand into global markets.

Notably, BYD — one of the world’s largest EV manufacturers — is also active in electric heavy-duty trucks, particularly in regional and logistics segments. Their absence from both the 600 km and 500 km tables is intentional. Today, most BYD heavy trucks are optimised for urban, port, and depot-based operations rather than articulated long-haul duty cycles, whether long-haul or regional line-haul. In other words, they dominate a different battleground.

That does not diminish their impact. With deep battery integration, massive manufacturing scale, and global deployment experience, BYD is already one of the most important players in electric freight. As those capabilities move up into the 600–800 km class, they have the potential to compress costs and accelerate the transition even further.

This is no longer a question of if. It’s happening everywhere, all at once.

The Myth of the 600 km Threshold

There’s a psychological barrier at 600 km. It feels like the moment electric trucks finally become “real”, the point where they match diesel expectations without compromise. But freight doesn’t run on psychology, it runs on routes.

A huge portion of global trucking sits in the 200 to 500 km range. Depot-based, predictable, repeatable runs that return to base daily. And in those environments, electric trucks never needed 600 km to win.

They were already ahead on the fundamentals. Lower energy costs, lower maintenance, higher uptime, and far less exposure to fuel volatility.

That’s the part most people miss. The disruption didn’t start when range hit a headline number. It started quietly, in the most boring routes in the system, where economics beat perception long before the narrative caught up.

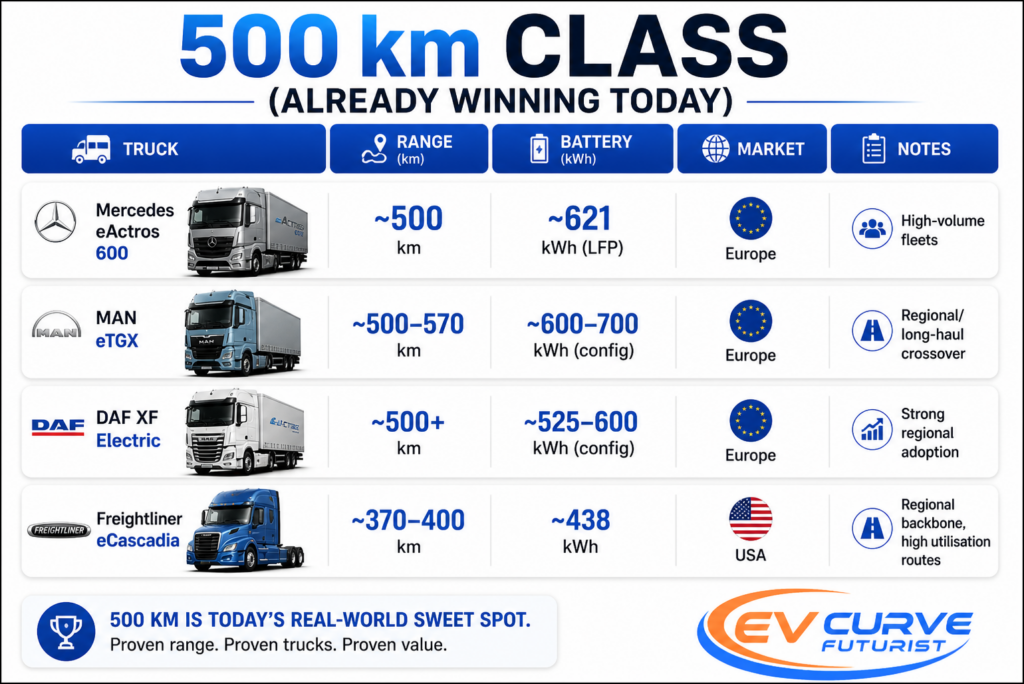

The Trucks That Are Already Winning

Trucks like the Mercedes eActros 600, MAN eTGX, and DAF XF Electric sit just below the 600 km mark.

On paper, they look like they fall short.

In reality, they are already replacing diesel across regional freight networks.

Because fleets don’t buy trucks based on maximum range.

They buy based on cost per kilometre, reliability, and how well a vehicle fits into existing operations.

If a truck can complete its route, return to base, and recharge overnight at a lower cost than diesel, the decision is already made.

That’s why the transition doesn’t begin at 600 km.

It accelerates below it.

Infrastructure and Utilisation Reality

Before long-haul fully flips, two constraints need to be acknowledged clearly.

First is charging infrastructure. The Megawatt Charging System (MCS) is the enabler for 600–800 km class trucks, but corridor coverage is still early. The vehicles are ahead of the network today.

Second is asset utilisation. Diesel trucks can run nearly continuously with team drivers. Electric trucks introduce charging windows that can reduce utilisation on certain long-haul routes. Over a week, that can translate into lost revenue if not planned correctly.

But both constraints are operational, not fundamental.

Infrastructure scales with demand and capital. Depot charging, corridor buildouts, and co-located solar and storage systems are already addressing this. Battery degradation is a valid consideration for fleets, but modern thermal management and manufacturer warranties are increasingly covering 800,000 km or more, aligning with typical heavy-duty asset lifecycles.

Utilisation shifts from maximum uptime to optimised routing. High-mileage, repeatable corridors, drop-and-hook or depot-to-depot relay models, and scheduled charging reshape operations rather than constrain them.

This is the phase the industry is entering right now.

Long Haul Is the Final Piece

Long-Haul Specs Snapshot

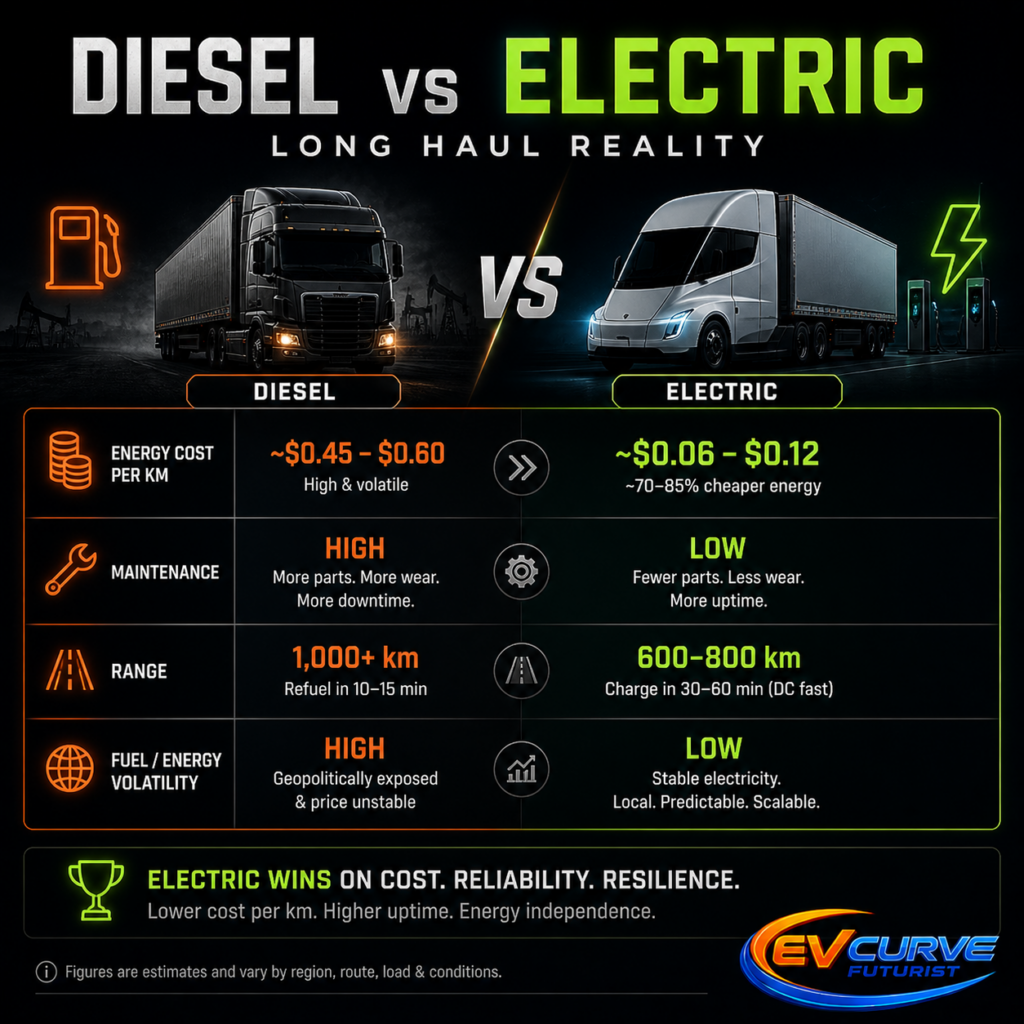

Where 600 km and above really starts to matter is flexibility. Long-distance freight corridors, intercity routes, operations where planning constraints matter just as much as cost. This is where trucks like the Tesla Semi and the new generation of European long-range electrics remove the final excuse for diesel.

Once range is no longer a limitation, the comparison becomes brutally simple. Energy cost, maintenance, risk. Electricity is cheaper and far more stable than diesel. Electric drivetrains have fewer moving parts, which means less downtime and higher utilisation. And critically, there’s no exposure to oil price shocks, supply disruptions, or geopolitical choke points.

At that point, diesel isn’t competing with electric. It’s being outclassed.

This is also where battery chemistry starts to matter. The Windrose EV Truck leans heavily into LFP, which gives it a real edge in cycle life, safety, and predictable degradation. In high-mileage freight use, that matters more than chasing maximum range on a spec sheet. They’re already talking about moving toward LMFP next, which could lift energy density while keeping that durability advantage. By comparison, many of the newer European trucks from Volvo Trucks are still largely built around NMC chemistries. Great for energy density, but not the same long-life, high-cycle profile you get from LFP. Different philosophies, different trade-offs.

At 150,000 km per year, the lifecycle math starts to flip hard. Diesel engines typically need major rebuilds in roughly 5–8 years, while LFP batteries are tracking toward 10–16+ years of usable life. The battery isn’t the weak link here by a million miles. The combustion drivetrain is. At high utilisation, diesel engines are more likely to need major rebuilds before LFP batteries wear out.

Zoom out and the direction is obvious. This isn’t theoretical anymore. Freight has moved into its final, operational phase.

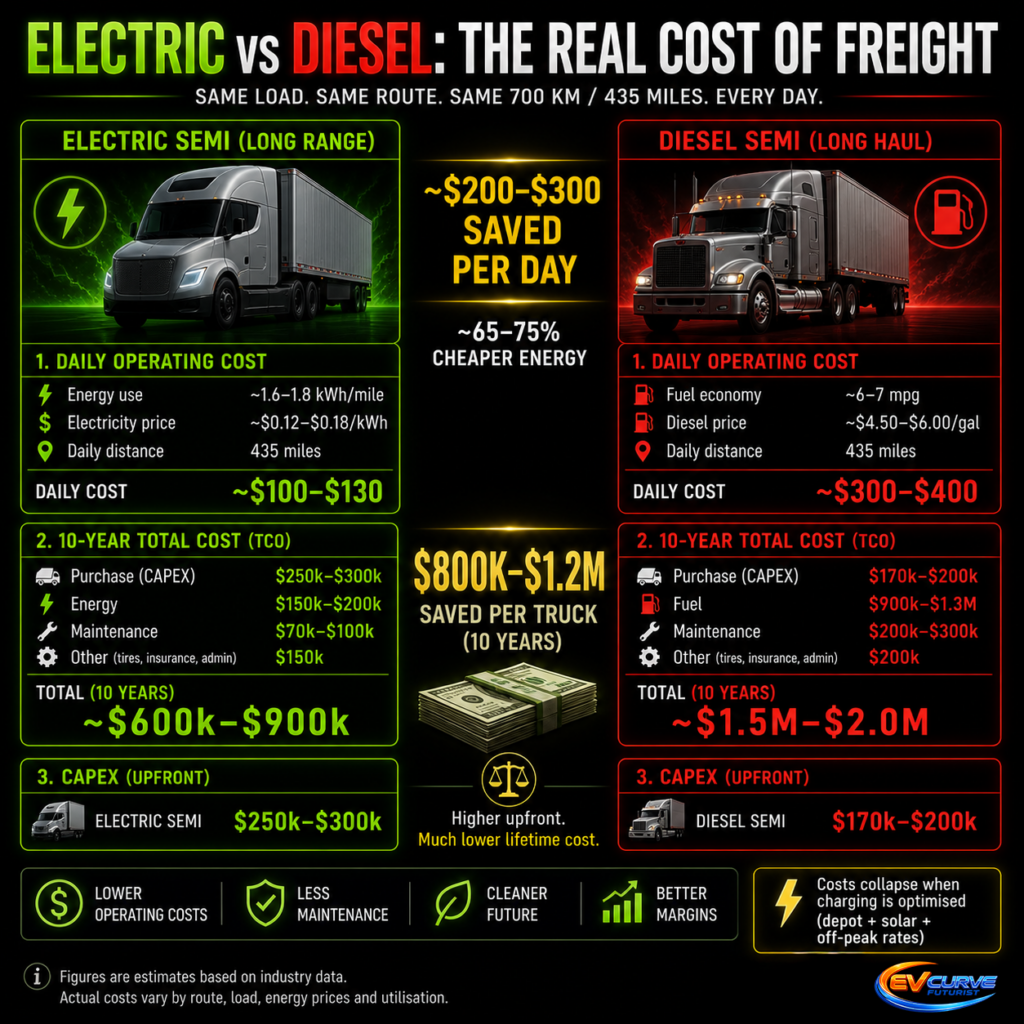

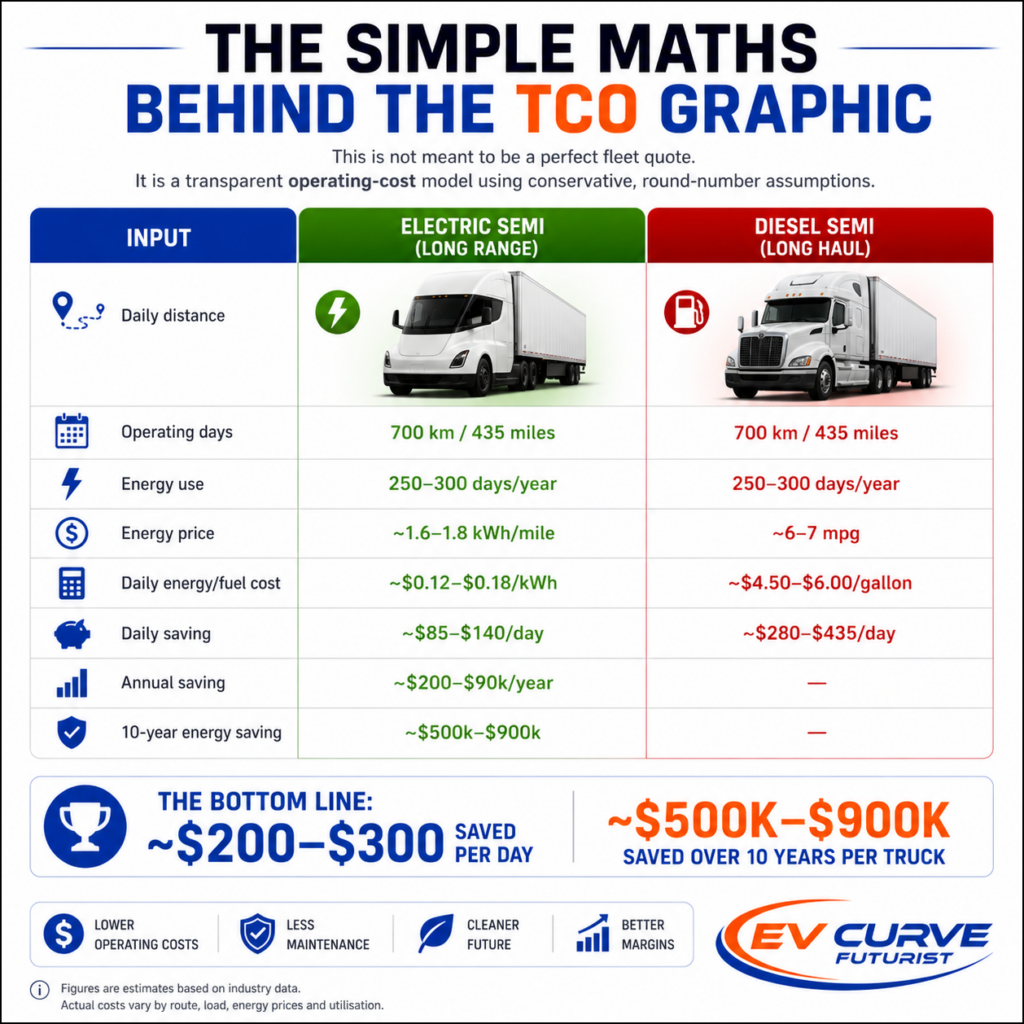

The Economics That Actually Decide

Assumes ~700 km daily, ~250–300 operating days/year. Figures vary by route, load, energy pricing and utilisation.

The Simple Maths Behind the TCO Graphic

This is not meant to be a perfect fleet quote. It is a transparent operating-cost model using conservative, round-number assumptions.

The fuel maths is straightforward.

For diesel: 435 miles ÷ 6–7 mpg = roughly 62–73 gallons per day. At $4.50–$6.00 per gallon, that is about $280–$435 per day in fuel.

For electric: 435 miles × 1.6–1.8 kWh/mile = roughly 696–783 kWh per day. At $0.12–$0.18 per kWh, that is about $85–$140 per day in electricity.

That means the electric semi saves roughly $200–$300 per day on energy alone, before lower maintenance, less downtime, and better fuel-price certainty are included.

Even if the electric truck costs $80,000–$120,000 more upfront, the energy savings can overwhelm that gap within the first few years on high-utilisation routes. That is the core point. The win is not theoretical. It is arithmetic.

Once range is no longer the constraint, the real battle becomes impossible to ignore. Not performance. Not branding. Not perception. Cost. On the same route, with the same load, running the same daily distance, the difference between electric and diesel is not marginal.

It’s structural. Energy costs collapse. Maintenance drops. Exposure to fuel volatility disappears. Over a single day, the savings are already meaningful. Over a decade, they become overwhelming. This is the moment the industry shifts. Not when electric trucks match diesel. But when they become significantly cheaper to operate at scale.

Because once that happens, the decision is no longer technical. It’s financial.

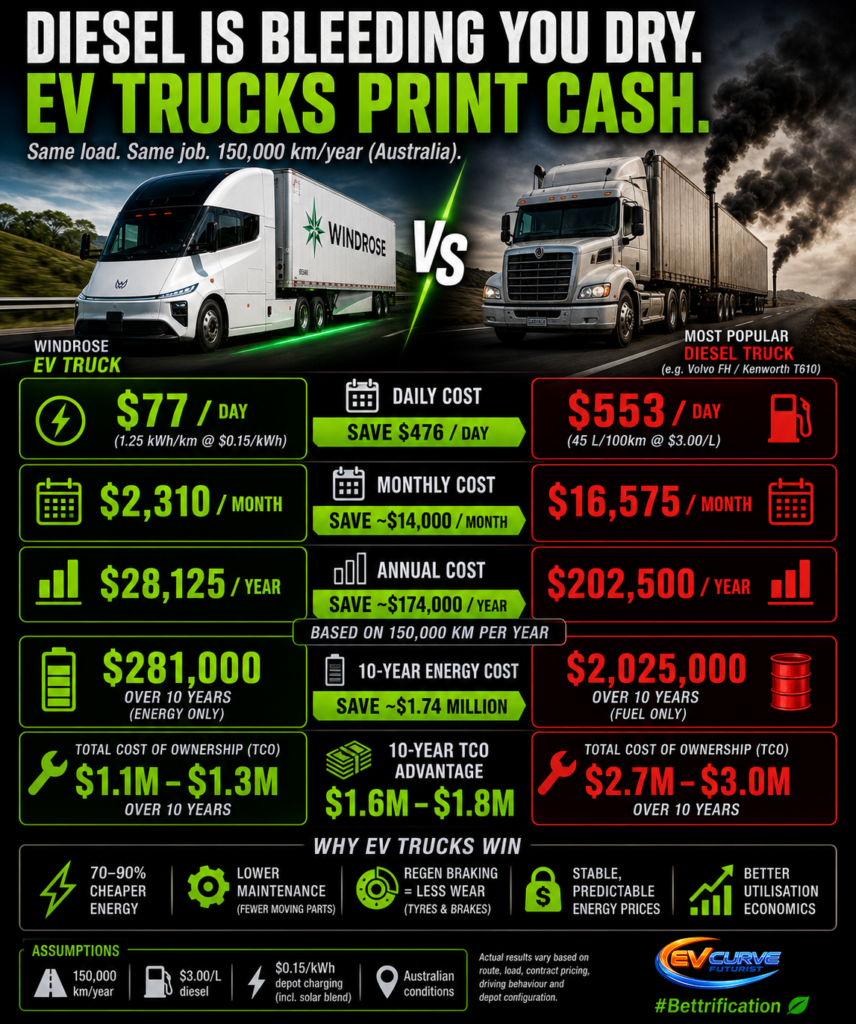

Now bring that into an Australian context and the picture sharpens even further.

On a typical 150,000 km per year route, diesel trucks are burning around 40 to 45 litres per 100 km. At roughly $3.00 per litre, that lands you north of $200,000 per year in fuel alone. That is before you even touch servicing, downtime, or component wear.

An electric truck running the same route sits in a completely different cost structure. At around 1.2 to 1.4 kWh per km, you are looking at roughly 180,000 to 210,000 kWh per year. At depot charging rates around $0.10 to $0.20 per kWh, especially with solar and storage in the mix, that comes in closer to $20,000 to $40,000 per year.

Same job. Same distance. Completely different economics.

And this is where it becomes undeniable. The savings are not coming from one lever. They stack. Energy collapses, maintenance drops, utilisation improves, and price volatility gets stripped out of the equation entirely.

Over a single year, the gap is already massive. Over a decade, it becomes decisive.

At that point, the question is no longer whether electric trucks can do the job.

It is why you would keep paying a premium to run diesel.

This Isn’t a Technology Story

This is not a technology story. It is a systems story.

The United States is pushing the frontier on range and charging infrastructure, led by Tesla’s vertically integrated approach.

Europe is leading in deployment, regulation, and fleet adoption, with established OEMs electrifying entire product lines.

China is scaling manufacturing and driving costs down, preparing to export long-range electric trucks into global markets.

Different strategies.

Same direction.

Freight Is Decoupling From Oil

For over a century, freight has been tied to oil — a long, complex, and volatile chain of extraction, refining, distribution, and combustion. Electric trucks break that link. Energy can be generated locally, stored, managed, and optimised, turning freight into an energy system rather than a fuel dependency. Solar, batteries, and depot charging collapse complexity and remove exposure to global fuel markets. This is not just about emissions. It is about control.

What This Means for Fleet Operators

- The transition does not start with long haul. It starts with repeatable, medium-mileage routes.

- Depot charging is the first unlock. Corridor charging is the second.

- Total cost of ownership already favours electric in regional freight.

- Range anxiety is being replaced by infrastructure planning.

- The question is no longer if fleets electrify, but how fast they execute.

The Real Inflection Point

600 km used to be the goal. Now it’s the baseline. The real inflection point wasn’t when electric trucks matched diesel range, but when they started beating diesel economics. That has already happened, and once cost curves move, everything else follows. Because in freight, like every industry facing disruption, cost, reliability, and predictability ultimately decide. Electric already wins on all three for most routes. And long haul is next.

Explore the Trucks (Specs & Enquiries)

For readers who want to dig into specs, configurations, and fleet enquiries, here are official manufacturer pages:

- Tesla Semi

- Volvo FH Aero Electric

- Scania Battery Electric Trucks

- Renault Trucks E-Tech T

- IVECO S-eWay Artic

- Windrose E700

- SANY Electric Trucks

These are not concepts or distant roadmaps. They are real products, available now or entering service across major markets.

The transition is no longer theoretical. It is already underway.