Why lithium investors keep getting psychologically destroyed at both the top and the bottom of the cycle

For those newer to the lithium space, the past few years probably looked completely insane.

One minute lithium was being called the most important commodity on Earth, with prices screaming toward 600,000 CNY/t and developers receiving billion-dollar valuations seemingly overnight. The next minute the entire sector was declared dead, structurally broken and permanently oversupplied as prices collapsed below 60,000 CNY/t and sentiment evaporated.

As someone who has been a lithium bull since 2017, I’ve lived through every phase of this cycle personally: the excitement, the euphoria, the fear, the doubt, the ridicule, the capitulation and now, finally, the early signs of renewed optimism.

What became obvious through this journey is that commodity cycles are rarely driven purely by fundamentals. They are driven by psychology. Sentiment overshoots reality in both directions. At the top, markets extrapolate shortages forever. At the bottom, they extrapolate oversupply forever.

Reality usually sits somewhere in between while the underlying disruption keeps advancing in the background.

That’s exactly what happened with lithium.

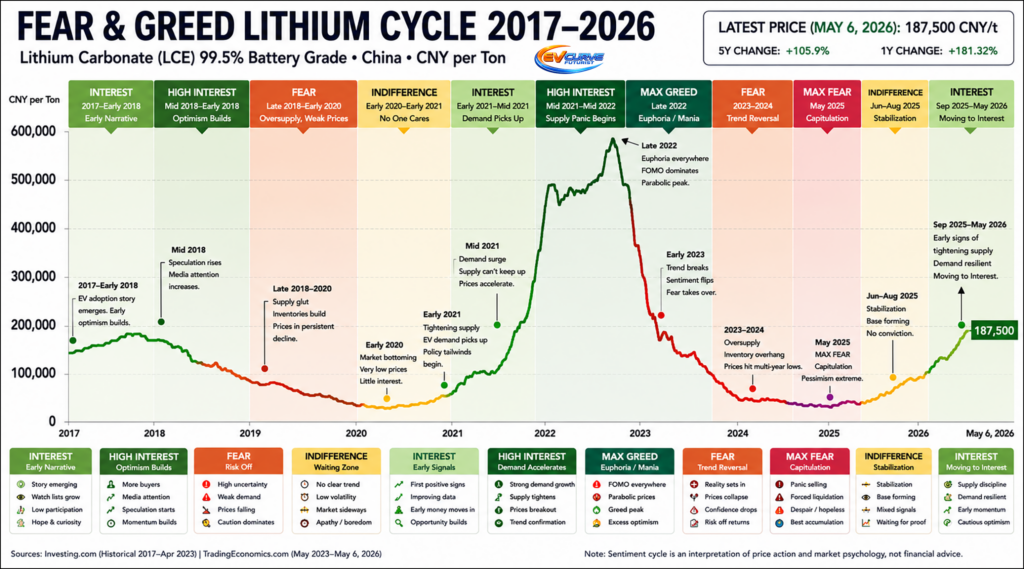

The Seven Emotional Stages of the Lithium Cycle

The Fear & Greed Lithium Cycle graphic was designed to map not only lithium price action, but the emotional psychology driving the cycle itself. In commodities, sentiment often matters just as much as fundamentals.

1. Interest (2016-2017 & 2021)

The first signs appeared between 2016 and 2017 as the EV story began emerging globally. Tesla was still proving EVs could work at scale, China was ramping battery production aggressively and investors started recognising lithium as a strategic material rather than a niche industrial commodity. Optimism built slowly as the first signs of structural change became visible. Most investors remained sceptical, but a growing minority sensed something important was happening beneath the surface.

A similar phase returned during 2021 as lithium recovered from the COVID-era downturn and investors once again began paying attention to tightening battery supply chains.

2. High Interest (2017-Early 2018 & Late 2021-Mid 2022)

As EV adoption accelerated and media coverage intensified, lithium entered a momentum phase. Speculation surged, retail participation exploded and developers attracted increasingly aggressive valuations as the market began pricing future shortages. Capital flowed freely into the sector and investor attention broadened rapidly.

The same pattern re-emerged in late 2021 and through much of 2022 as lithium prices surged and investors rediscovered the sector following the post-pandemic recovery.

3. Euphoria (Mid 2018 & Late 2022)

Confidence eventually became conviction. Valuations detached from fundamentals, risk was increasingly ignored and many investors assumed demand growth would overwhelm any future supply response.

This occurred first during 2018 and then again, even more dramatically, in late 2022 when lithium carbonate approached 600,000 CNY/t and the dominant narrative became simple: lithium shortages would last forever.

4. Indifference (Late 2018 & Early 2023)

Then reality arrived.

Both in late 2018 and again during early 2023, prices stopped rising, investor attention drifted elsewhere and enthusiasm faded. What had recently been one of the market’s most exciting themes suddenly became far less interesting.

5. Fear (2019 & Mid-Late 2023)

Throughout 2019 and again during the second half of 2023, falling prices and deteriorating sentiment caused investors to question whether the original thesis had been fundamentally flawed. Fear replaced conviction as oversupply narratives gained traction.

6. Panic (Late 2019-Early 2020 & 2024)

As downturns deepened, fear evolved into panic. Forecasts were cut, projects delayed and every headline appeared negative. Investors stopped asking how high prices might go and began wondering how much lower they could fall. Confidence collapsed alongside valuations.

7. Capitulation (Early-Mid 2020 & Late 2024-Early 2025)

At the deepest points of both downturns, many investors gave up entirely. Positions were sold regardless of price and the focus shifted from opportunity to damage control. Conviction disappeared and emotional exhaustion took over.

8. Despondency (Mid-Late 2020 & Much of 2025)

By 2020, lithium prices had collapsed toward multi-year lows near 40,000 CNY/t and the sector became effectively uninvestable in the eyes of most market participants. Retail disappeared, volumes dried up and analysts stopped paying attention. Even good news struggled to attract interest.

A similar mood returned through much of 2025 as the market remained focused on oversupply despite continued growth in EVs, battery manufacturing and energy storage.

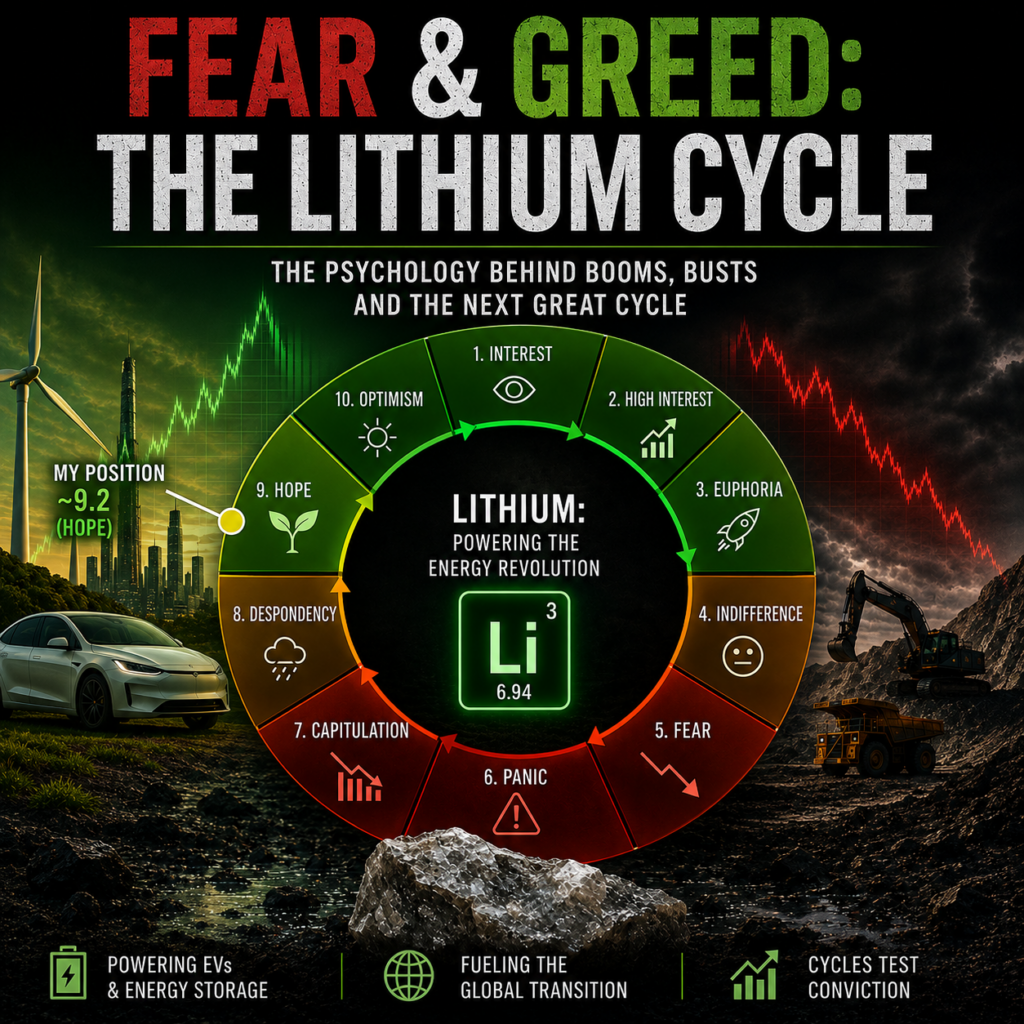

9. Hope (Late 2020-Early 2021 & Late 2025-May 2026)

Quietly, conditions began improving. Demand recovered, supply tightened and inventories started normalising. Most investors remained focused on the recent past, but the worst appeared to be over. The first signs of a new cycle were emerging long before the broader market noticed.

This is where I currently place the lithium market today.

10. Optimism (2021 & ?)

By 2021, tightening supply conditions and accelerating EV demand began feeding back into lithium pricing. At first, many investors viewed the rebound as temporary, but prices kept climbing as battery demand accelerated faster than producers could respond. New projects struggled to come online quickly enough and the market suddenly rediscovered an uncomfortable truth: lithium supply chains are not infinitely elastic.

Years of underinvestment had created bottlenecks.

Whether today’s Hope ultimately transitions into another period of Optimism remains one of the key questions facing lithium investors in 2026.

I currently place myself around 9.2 (Hope) – May 2026. The fundamentals look considerably stronger than sentiment suggests, with EV adoption, battery storage deployment and battery intensity all continuing to grow. At the same time, many lithium equities remain heavily discounted, mainstream interest is limited and the dominant narrative remains cautious. To me, that feels closer to hope than optimism, and a long way from the euphoria of 2022.

The Great Lithium Collapse

The decline between 2023 and 2025 was one of the most psychologically destructive periods lithium investors have ever experienced. Prices collapsed, developers got crushed and forced liquidations accelerated downside momentum as the narrative completely inverted from “shortages forever” to “permanent oversupply.”

Social media turned vicious, analysts downgraded the sector aggressively and retail investors capitulated. Many abandoned the space entirely.

The irony is that EV demand never stopped growing during the collapse. That’s the critical point most people missed. The demand side of the disruption story remained intact. What actually happened was a brutal cyclical washout. Supply surged too aggressively into the 2022 spike, while temporary inventory overhangs distorted market conditions and amplified the collapse. Weak projects got purged, speculative excess disappeared and sentiment imploded.

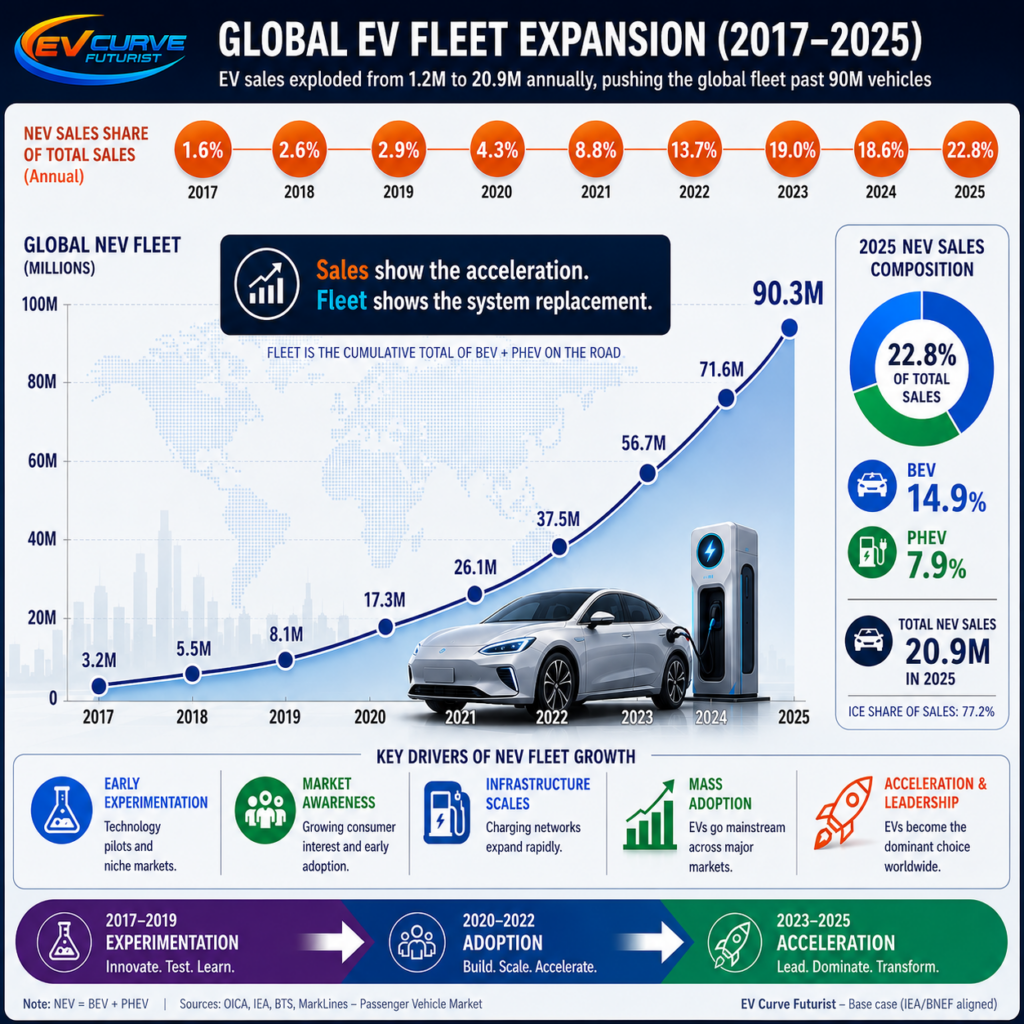

What looked insignificant in 2017 is now compounding into system-scale disruption. Annual EV sales surged from just 1.2M to 20.9M between 2017 and 2025, expanding the global EV fleet from 3.2M to more than 90M vehicles.

Sales show momentum, but fleet growth reveals the deeper story: millions of EVs permanently entering the global transport system each year, steadily reshaping oil demand, infrastructure, supply chains and the automotive industry itself.

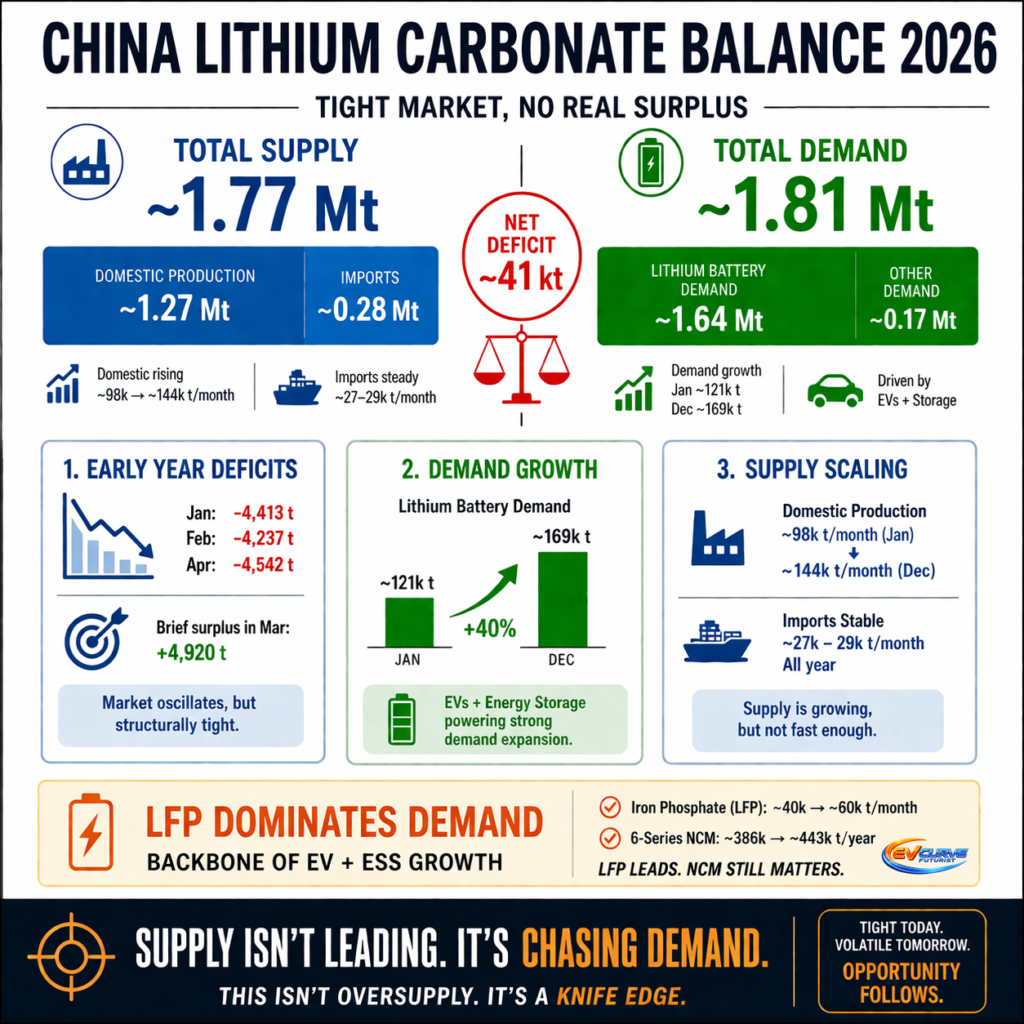

Beneath the panic, however, the structural balance was already beginning to tighten again. By May 2025, the sector reached what I believe was the true emotional bottom of the cycle. Not necessarily because prices hit their absolute lowest point then, but because psychologically the sector looked completely broken. This was the Max Fear phase, where investors stopped asking when lithium would recover and started asking whether lithium had a future at all.

Around this same period, China’s carbonate balances were quietly tightening while LFP deployment across EVs and ESS continued scaling rapidly.

The important point here is that the lithium market was never drowning in endless surplus the way headlines often suggested.

Even in 2026, China’s carbonate balance appears structurally tight, with demand (~1.81 Mt) already slightly outpacing supply (~1.77 Mt). The market oscillates month to month, but the broader trend shows demand continuing to accelerate faster than supply can comfortably respond.

That distinction matters.

Supply is still scaling aggressively, particularly domestic Chinese production, but battery demand driven by EVs and ESS continues compounding at extraordinary speed. LFP remains the dominant chemistry powering that expansion, especially across mass-market EVs and stationary storage.

In other words, supply isn’t really leading the market anymore. It’s chasing demand.

And when markets transition from apparent surplus toward structural tightness, sentiment often changes far faster than most participants expect.

That’s usually how bottoms form.

Why The Thesis Never Actually Broke

Before continuing, it’s important to acknowledge that many veteran commodity investors who have lived through multiple full resource cycles may disagree with parts of this framework or interpret the current lithium market differently. That’s fair. Commodity markets are notoriously difficult to model because timing, supply elasticity, geopolitics and sentiment all interact unpredictably. This article simply reflects my interpretation after following the sector closely since 2017.

One of the biggest misconceptions during the collapse was the idea that lithium demand itself had failed. That simply wasn’t true.

The broader Bettrification thesis kept advancing the entire time. For those unfamiliar with the term, Bettrification is my shorthand for the accelerating shift toward a battery-powered world, combining electrification, batteries, software, automation, AI and renewable energy into one converging disruption thesis where batteries increasingly sit at the centre of transport, energy storage, AI infrastructure and eventually large parts of industrial society itself.

EV adoption continued growing globally, China accelerated electrification, grid-scale storage deployment exploded and LFP batteries became increasingly dominant. The world kept moving toward electrification even while lithium equities were being obliterated. Short-term oversupply does not automatically invalidate long-term structural demand. The market temporarily confused cyclical imbalance with thesis failure. Those are not the same thing.

Sodium-Ion, LMFP and the Future

Rising lithium prices will inevitably accelerate investment into alternative battery chemistries. Sodium-ion batteries are real technology with genuine potential, particularly in lower-cost stationary storage and entry-level EV applications, and major players like CATL and BYD are already pushing aggressively into sodium development.

But scale matters. Sodium production capacity remains tiny relative to lithium, and scaling global manufacturing to meaningful levels will likely take years. In transport applications, weight and energy density still matter enormously as consumers continue demanding longer range, faster charging, better efficiency and lighter vehicles.

That reality continues to favour LFP in the near term and likely LMFP as the next major evolutionary step. Sodium will absolutely carve out market share, especially in ESS and lower-end mobility, but the idea that it suddenly replaces lithium entirely misunderstands both manufacturing scale and battery physics. The battery ecosystem will likely become increasingly diversified rather than fully replaced.

A Trend Few Forecasts Are Talking About

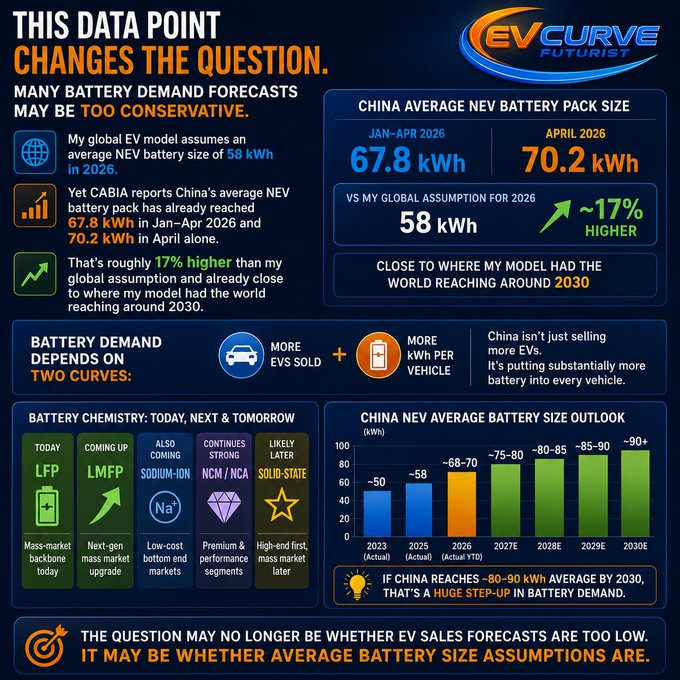

Source: CABIA (China Automotive Battery Innovation Alliance), Jan-Apr 2026 battery installation report.

One data point recently made me question whether some lithium demand forecasts remain too conservative.

My own global EV model assumes an average NEV battery size of 58 kWh in 2026. Yet CABIA reports China’s average NEV battery installation reached 67.8 kWh during January-April 2026, with April alone reaching 70.2 kWh. That’s roughly 17% higher than my assumption and already approaching where my model had the world reaching around 2030.

Importantly, these figures reflect China’s broader NEV market, including passenger vehicles, buses, trucks and commercial vehicles. That arguably makes the trend more significant, not less. It suggests electrification is spreading into larger vehicle categories that consume substantially more battery material per unit.

This trend is particularly interesting given Benchmark Mineral Intelligence’s recent forecast for lithium markets to move from deficit in 2026 to a modest surplus in 2027 as supply disruptions resolve and new production arrives. On paper, the logic is straightforward: mines ramp, restarts succeed, bottlenecks ease and supply grows faster than demand.

The real world is rarely that tidy.

Commodity forecasts often assume supply arrives broadly on schedule and demand evolves in a relatively linear fashion. Yet history suggests both sides of the equation are usually messier. Projects slip, ramps disappoint, permitting takes longer than expected and logistical constraints emerge. Meanwhile demand continues evolving. Larger battery packs, expanding commercial vehicle electrification and rapidly growing energy storage deployments can all increase lithium consumption faster than vehicle sales alone might suggest.

The purpose of this observation isn’t to suggest Benchmark is wrong. Rather, it highlights how sensitive future balances may be to assumptions that appear reasonable today. Small changes in battery intensity, storage deployment or supply execution can have an outsized impact on the final outcome.

The question may no longer be whether EV sales forecasts are too low.

It may be whether both supply and demand assumptions are too neat for a rapidly changing industry.

The Most Important Lesson

The biggest lesson from the lithium cycle has very little to do with lithium itself. It’s about psychology. Markets always sound smartest at the extremes: at the top, “shortages forever”; at the bottom, “permanent oversupply.” Neither narrative fully captures reality. The truth usually sits somewhere in between while disruption steadily compounds underneath the noise.

The lithium cycle was never just about lithium. It was a real-time psychological stress test for belief in the broader Bettrification thesis itself.

Now, after nearly four years of pain, tightening conditions are finally beginning to re-emerge and the market appears to be entering the next emotional phase once again. Not euphoria. Not mania. Just early interest.

The key signals I’ll be watching are whether lithium carbonate can sustainably hold above the ~180,000–200,000 CNY/t range for several consecutive months while China continues reporting tightening carbonate balances, alongside EV battery installations consistently remaining above ~80 GWh/month as port inventories tighten further.

Should those conditions persist simultaneously, it would strongly suggest the market is moving beyond simple cyclical recovery and back toward structurally constrained conditions, potentially marking the beginning of the next genuine High Interest phase of the cycle.

And cycles usually begin quietly before they become obvious to everyone.

Disclaimer: This article reflects personal views and interpretations of market cycles and sentiment. It is not financial advice.